Poverty reduction through the development of inclusive food value chains

2021-03-23RobVOSAndreaCATTANEO

Rob VOS,Andrea CATTANEO

1 International Food Policy Research Institute (IFPRI),Washington,D.C.20007,USA 2 Food and Agriculture Organization of the United Nations (FAO),Rome 00153,Italy

Abstract Propelled by urbanization,rising incomes,and changing diets,food markets have been expanding in Africa and South Asia,creating the vast potential for job and income opportunities along food supply chains and,hence,for poverty reduction. The novel coronavirus (COVID-19) that spread to a pandemic in early 2020 provokes enormous setbacks to this expansion. This,however,should provide lessons regarding the importance of resilient and inclusive food systems. Emergency responses to COVID-19 should consider interventions towards that end and leverage the opportunities provided by food markets growth as economies recover from the present economic recession. This paper assesses options of how this could be done by facilitating the better functioning and interconnectedness of the many small and medium-sized enterprises that are proliferating along the “hidden middle” of food value chains in storage,logistics,transportation,and wholesale and retail distribution. It also explores how policies can help smallholder farmers connect to this “hidden middle” in more gainful ways and help them climb out of poverty as well.

Keywords:poverty,food security and hunger,food supply chains,South Asia,sub-Saharan Africa

1.lntroduction

Economic progress in developing countries since the 1990s has lifted more than 1.2 billion people out of extreme poverty-defined as living on less than purchasing power parity(PPP) 1.90 USD a day -between 1990 and 2015 (World Bank 2020). Yet,by the latest World Bank estimates,there were 735 million people in extreme poverty worldwide by 2015,most living in the rural areas of sub-Saharan Africa and South Asia. The global economic recession and supply chain disruptions caused by the outbreak of the COVID-19 pandemic in early 2020 threatens to pose enormous setbacks in reducing hunger and poverty,severely affecting vulnerable people,especially in these poorest regions (FAO 2020; Labordeet al.2020). Hence,also when looking beyond COVID-19,reducing poverty and ending hunger depend on making progress in rural areas in these regions.

This paper contributes to three fronts. First,it highlights the gains that have been made in reducing poverty in rural areas. Second,the paper discusses the role of boosting smallholder productivity and incomes,and creating off-farm employment by developing the downstream segments of food value chains that can achieve the same for those who have remained behind. Third,it presents concrete policy options to leverage agri-food system transformation for greater inclusion of smallholder households and other rural people. In this paper,we see inclusive food systems as those that also allow poor and vulnerable groups to engage in food system activities and earn a fair share in the value added generated in food supply chains. An inclusive food system is also one that enables access to affordable,safe,and nutritious foods for all people,including poor consumers.

Food markets have both changed and expanded rapidly in sub-Saharan Africa and South Asia prior to COVID-19.Even as the lasting impacts of COVID-19 are difficult to discern at the time of writing (July 2020),there is,for now,no reason to assume those trends would fundamentally change during and after the recovery from the present global downturn. This implies that we should expect the enormous potential for job and income opportunities along food supply chains to still be out there post-COVID-19. Over the past decades,food market growth in the poorest regions has been propelled by urbanization,rising incomes,and changing diets. In both sub-Saharan Africa and South Asia,this has opened space for the emergence of a proliferation of small and medium-sized enterprises (SMEs) in storage,logistics,transportation,and whole and retail distribution to meet the growing rural and urban food demand. These middle segments of the food chain are often referred as“hidden middle”,as its importance tends to be overlooked in data systems and by policymakers. This “quiet revolution”in the “hidden middle” of African and Asian food systems appears to be happening outside the view of policymakers.As a result,much of the potential for leveraging inclusive value chain development is left untapped. To leverage inclusive food supply chain development,we recommend that policymakers recognize the major transformations in downstream activities. Two sets of key recommendations for inclusive food system development follow from here.First,policies should focus on facilitating the development of the “hidden middle” of agri-food supply chains by (1)providing adequate basic infrastructure (roads,electricity,information and communications technology (ICT)connectivity); (2) creating the right market incentives and food standard regulation; (3) facilitating skills,especially for entrepreneurship and adoption of quality standard and use of ICT; and (4) creating vehicles for more inclusive value chain finance and business services. Second,smallholders’ insertion into dynamic food supply chains would be greatly helped by (1) strengthening land tenure security and improve their access to finance,inputs,and ICT;(2) facilitation of the development of inclusive agribusiness models,such as cooperatives and producer organizations for smallholders; (3) skills training and technical assistance to enable smallholders to comply with food safety and quality standards of modern supply chains; and (4) designing social protection programs so that they help farmers and non-farm rural households manage market shocks and other risks,strengthen their resilience (including through improved nutrition) and enable diversification to non-farm rural activity.

The focus on the transformation of the agri-food system at large is a key contribution of this paper in the context of the broader literature on agricultural transformation and poverty reduction. The traditional economic development literature focused on the structural transformation of economies from having agriculture as the mainstay to more dynamic productivity and income growth pushed by modern industry and services. Economic growth would tend to be more inclusive if the transformation would be “pushed” in its initial stages by strong agricultural productivity growth to facilitate rural income growth,low food prices,and resource transfers enabling both poverty reduction and employment growth in urban,non-agricultural sectors (e.g.,Timmer 1988;Ocampo and Vos 2008). In this paper,we argue that such outcomes would strongly depend on the inclusiveness and dynamics of the entire agri-food system; hence,it would not only depend on the productivity growth of the agricultural sector itself but the way the rest of the agri-food system(especially the “hidden middle”) is developed,as analyzed in recently published literature (Reardon and Timmer 2014;FAO 2017; Barrettet al.2019; Vos 2019).

The remainder of this paper is organized as follows.In Section 2,we identify the challenges of global poverty reduction,how they relate to ongoing processes of agricultural transformation and food system change,and how COVID-19 is affecting poverty and food security. In Section 3,we analyze options for leveraging food systems to boost incomes and create jobs for smallholders and rural workers through proven ways to promote non-farm job creation and income generation,especially through development of the “hidden middle” of agri-food supply chains. In Section 4,we review options for making food supply chains more beneficial to the hundreds of millions of mostly poor smallholders through inclusive agribusiness models,enabling policies that help connect them to markets,and appropriate territorial planning of food system development. Section 5 concludes.

2.Poverty,agricultural and rural transformations,and food system change

2.1.Rural transformation and poverty reduction

Industrialization,which has been the main driver of past structural transformations,lags in most countries in sub-Saharan Africa and South Asia. In these impoverished regions,rapid urbanization is not commensurate with the growth in employment and income opportunities witnessed in manufacturing and modern service sectors. As a result,most workers exiting low-productivity agriculture are moving into low-productivity informal services,usually in urban or peri-urban areas. The benefits of this type of transformation are modest. Since the 1990s,poverty rates in Africa have declined little,while the absolute number of poor has risen(World Bank 2018). Poor rural Africans migrating to cities are more likely to join the masses of urban poor than to find a pathway out of poverty. A similar dynamic is happening in South Asia,where the rural poor are more likely to escape poverty by staying in rural areas than by moving to cities(FAO 2017).

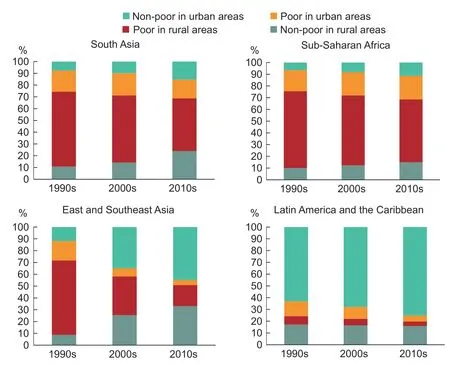

Fig.1 confirms that progress in rural areas has been central to poverty reduction and will be central also to achieving the first SDG of eradicating poverty. The figure draws from FAO (2017) and is based on World Bank data for 27 countries with a combined population of over 4 billion.It shows regional trends in urban and rural poverty in the last two decades.

Rural poverty has been substantially reduced in the last two decades only in East and Southeast Asia,where the share of the rural non-poor in total population increased from 9% in the 1990s to 33% in the 2010s,while the share of all poor fell from 79 to 22%. Although the initial poverty rates in South Asia and sub-Saharan Africa were comparable with those of East and Southeast Asia,the shares of urban and rural poor in both regions have been only modestly reduced.

Evidence from the literature demonstrates that the patterns and the speeds of structural and rural transformations differ widely by region and,in many cases by country,leading to considerable differences in welfare outcomes. In East and Southeast Asia,such transformations strengthened linkages between urban and rural economies,which contributed significantly to poverty reduction. Productivity improvements in agricultural and non-agricultural sectors have reduced the total number of poor,both urban and rural,by more than 800 million since the 1990s. In contrast,in South Asia,where agriculture is still the principal employer and population growth rates are higher than those of the East and Southeast Asian countries in the sample,at 23 million,the reduction in the number of poor between 1990 and 2015 has been modest (FAO 2017). During this period,a larger share of people exited poverty in South Asia while remaining in rural areas than those that exited poverty in urban areas.

Fig.1 Changes in shares of rural and urban poor and non-poor in the total population of selected developing countries by region,1990s and 2010s. For ease in comparison of country cases that differ widely by the level of income per capita,the poverty level used is “moderate”,defined as living on less than 3.10 USD a day (measured in 2011 purchasing power parity,PPP). The charts refer to the following countries,selected for data availability:East and Southeast Asia -Cambodia,China,Indonesia,Philippines,Thailand,Vietnam; South Asia -Bangladesh,Nepal,India; Latin America and the Caribbean -Brazil,Colombia,Dominican Republic,Guatemala,Nicaragua,Peru; Sub-Saharan Africa -Burkina Faso,Côte d’Ivoire,Ethiopia,Mali,Malawi,Mozambique,Nigeria,Rwanda,South Africa,Uganda,United Republic of Tanzania,and Zambia. Source:Taken from FAO (2017; Fig.2).

In contrast,in Latin America and the Caribbean,recent poverty reduction has been pushed by the dynamics in urban areas. This should not be surprising,as,by the early 1990s,urbanization was already high,and poverty rates were low in this region. Between 1990 and 2015,the countries in Latin America and the Caribbean witnessed,on average,strong agricultural productivity growth,but this did not contribute to significant poverty reduction in rural areas,as a result of wide inequalities in land distribution and in the valueadded sharing along agri-food supply chains. The number of extreme poor in Latin America’s rural areas fell by only 2 million,from 41 to 39 million,between the late 1980s and 2015 (Anríquez 2016).

One further finding that emerges from Fig.1 is that,in all regions,economies of rural areas are just as important a contributor to lifting people out of poverty as those of urban areas are. This is in part due to the larger proportion of the poor who live in rural areas,but also to the fact that,whether through agriculture or non-farm employment,many rural poor are improving their incomes and exiting poverty. The key message to policymakers is that resources need to be allocated to rural areas not just because that is where most of the poor are but because their economic development can help reduce high levels of migration and poverty in urban centers. The linkages and interplay of rural areas with urban centers are critical,and investing to connect rural areas to the services,institutions,and markets provided by cities and towns is particularly important. Enhancing rural-urban linkages will be critical for making food systems more effective and inclusive,thus contributing to achieving multiple SDGs,especially those of ending poverty,hunger,and all forms of malnutrition.

The lack of cross-sectoral dynamics explains in good part why poverty reduction has been and is still so slow in sub-Saharan Africa:rapid urbanization is not supported by any significant expansion of manufacturing employment. As a result,people leaving agriculture are moving mostly into the informal service sector,characterized by low productivity.In such cases,instead of finding a pathway out of poverty,rural migrants are likely to join the ranks of the urban poor.A similar dynamic is seen in South Asia and where the rural poor are more likely to escape poverty by remaining in rural areas than by migrating to cities.

These driving forces of persistent poverty in sub-Saharan Africa and South Asia are likely to be exacerbated by COVID-19. Indeed,they are expected to hit the hardest where the mentioned weaknesses in food systems prevail.It increases the probability of severe supply chain disruptions from necessary social distancing measures. Together with spillover effects of the global economic downturn,this may push millions if not hundreds of millions of people below the extreme poverty line of PPP 1.90 USD per person per day. In one assessment,Labordeet al.(2020) estimate that a projected global economic downturn by five percentage points of GDP growth,as projected by the IMF in June 2020(IMF 2020),could lead to an increase in global poverty of 20%,affecting 148 million people. Most of the increase would affect the vulnerable in sub-Saharan Africa (80 million)and South Asia (40 million). This setback reiterates the importance of creating inclusive and well-integrated supply chains.

2.2.Agricultural transformation and the future of smallholder farming

Worldwide,about 1.5 billion people,many of them poor,live in smallholder households. What constitutes a small farm varies within and across countries. It depends on socio-economic and agro-ecological conditions,but in international comparisons,a threshold of 2 hectares is most often used to define “small”. According to a recent study by Lowderet al.(2019),worldwide,510 million farms (84% of an estimated total of 608 million farms) operate less than 2 hectares of agricultural land,while 70% of farms cultivate less than 1 hectare.

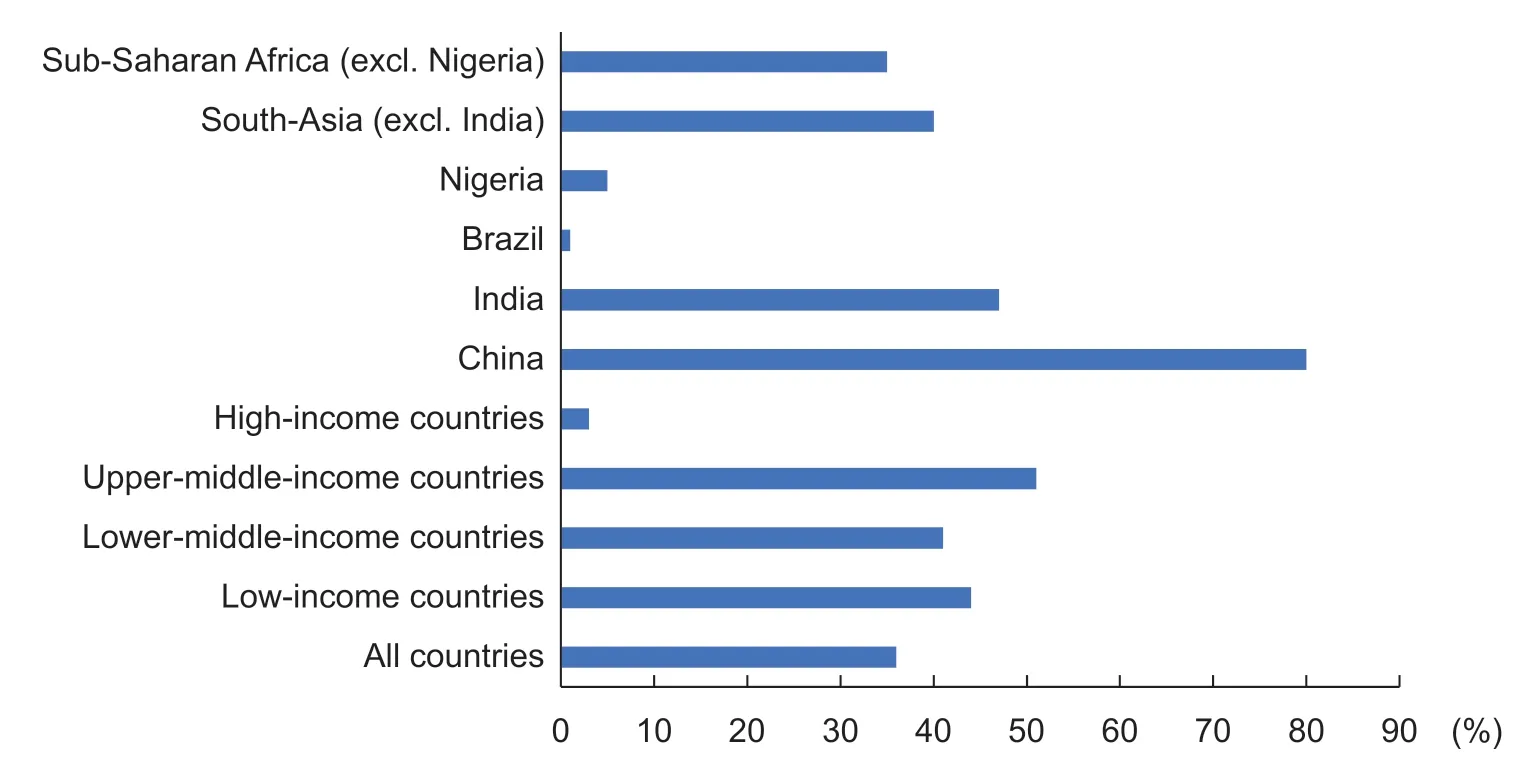

Despite their oft precarious position,smallholders play a large role in the food system. Worldwide,smallholders generate,on average,about 36% of the primary production value of domestic food production -significant,though far less than often claimed (Fig.2). In low-and middle-income countries,this share is somewhat higher at between 40 and 50%. In sub-Saharan Africa and South Asia (excluding India),smallholdings comprise 70 to 75% of farm units,but they generate just an estimated 35 to 40% of the primary production value of the domestic food sector. In India,the share is somewhat higher at 50%,but it is substantially larger in China,where smallholders produce about 80% of the value of the domestic primary food supply.

The aforementioned 36% of primary production value of domestic food production on small-sized farms utilizes only 11% of the world’s farmland,indicating relatively high land productivity amongst smallholders,confirming a widely held hypothesis (e.g.,Timmer 1988). However,their higher land productivity comes with much lower labor productivity (Mikecz and Vos 2016). Limited access to land and modern agricultural inputs,high reliance on labor,and concentration on inexpensive staple crop production explain the disproportionately low share of agri-food value added earned by small-scale farmers and their low labor productivity. Smallholders will likely continue to face these challenges in the near future,especially in terms of access to land. Enabling their more inclusive participation in food-sector growth has significant potential to overcome some of these challenges and reduce poverty and improve livelihoods.

Fig.2 Smallholder share in value of primary food production. Source:Lowder et al. (2019).

Smallholder participation in food and agriculture markets is increasing (HLPE 2013),and many smallholders supplement low farm-based revenue with income from off-farm work,often in the informal economy (FAO 2015b).Yet,poverty among smallholders remains higher than other socio-economic groups. About 80% of the world’s extreme poor live in rural areas,and 65% of them are dependent on (smallholder) agriculture for their livelihoods. In sub-Saharan Africa,these shares are 82 and 76%,and in South Asia,these are 83 and 56% (Castañedaet al.2016). When smallholders possess little land and human capital and live in isolated communities,they are likely to be poorly integrated into agri-food value chains and have limited access to markets,finance,and services (Hazell 2007).

Based on this evidence,achieving substantial productivity and income increases for smallholders (e.g.,SDG target 2.3 aims to double smallholder productivity by 2030) is essential for food security,given the high poverty incidence among smallholders. However,such productivity gains and income improvements will be illusory without better market access for smallholders,which in turn will require better integration and development of downstream parts of food supply chains.

2.3.Urban growth and food system change

Hence,to fully tap the potential of leveraging food systems for poverty reduction,more is needed than invigorating rural economies. This is the case in particular because moving forward,growing urban markets will be the main drivers of agri-food sector expansion,including in low-income Africa and Asia. Urban populations already consume up to 70%of the world’s food supply,even in countries with large rural populations (Reardon 2016). Income growth is driving a dietary transition,as urban consumers shift consumption from staple cereals toward high-value fish,meat,eggs,dairy products,fruits,vegetables,and processed foods.Growing demand for these high-value products provides an opportunity for agriculture. But it also presents challenges for millions of small-scale farmers. Expanding and increasingly profitable food markets can encourage the concentration of food value chains in large commercial farms and large-scale processors and distributors (supermarkets),possibly excluding smallholders. To benefit from market opportunities,small-scale producers will have to adjust to ongoing market changes and increasingly stringent food quality and safety requirements in downstream food value chain segments.

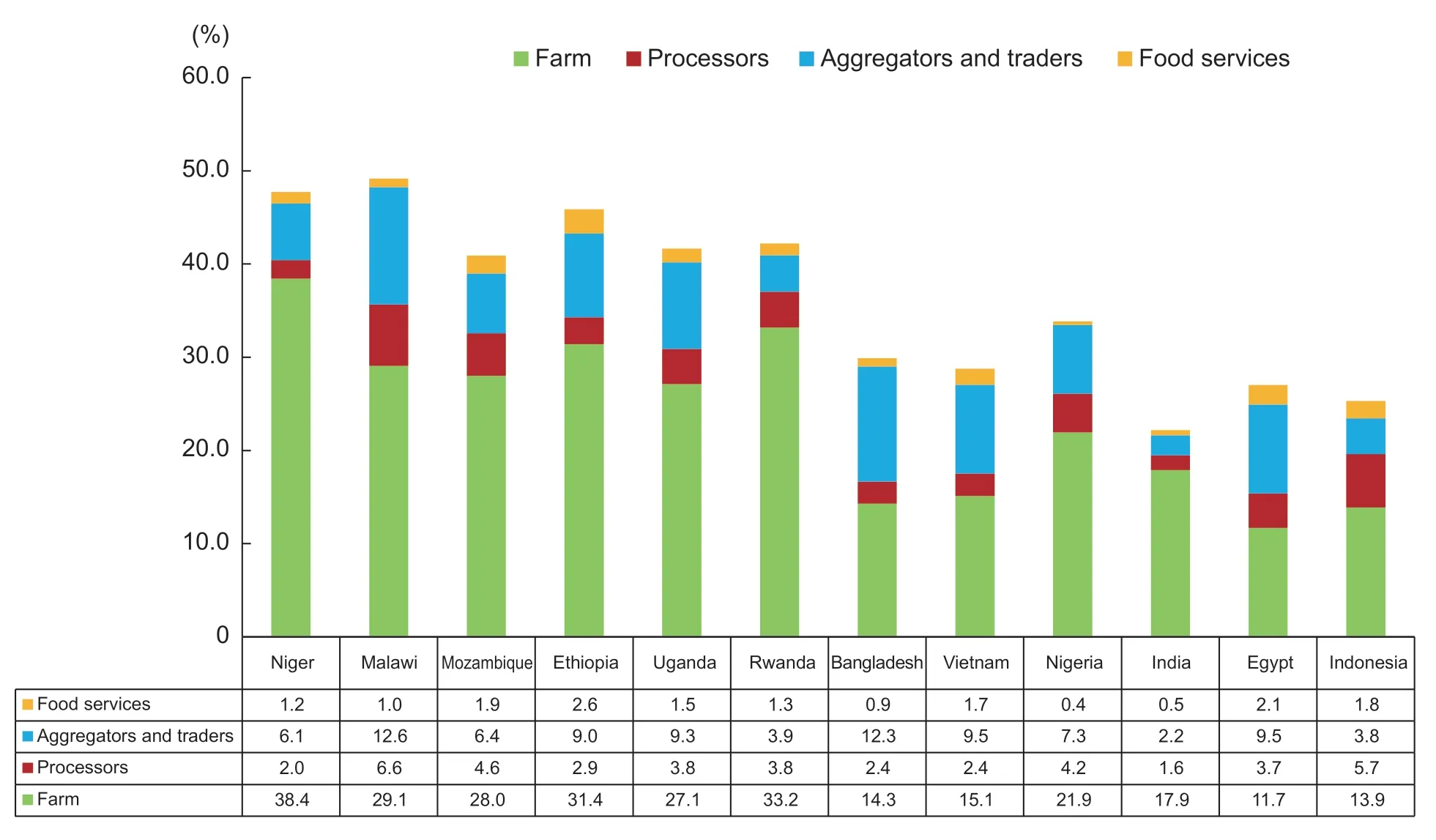

As the food system transforms,the emergence of millions of SMEs in transportation,processing,and distribution -the expanding “hidden middle” of the food supply chain -can promote the inclusion of the rural poor. As food processing,distribution,and services tend to be more labor-intensive,and labor productivity is relatively high in these sectors,the food and beverage industries have great potential for creating non-farm employment. For women,in particular,employment in high-value food sector activities has expanded considerably in many countries. In sub-Saharan Africa and South Asia,midstream activity now represents a substantial portion of agri-food sector GDP,ranging from 21% in low-income countries like Rwanda to around 50%in middle-income countries like Egypt and Indonesia (see Fig.3). Recent evidence shows that with access to improved infrastructure (roads,storage,electricity,and drinking water)and credit,SMEs can thrive and become instrumental in connecting farmers to markets (Barrettet al.2019; Reardonet al.2019a,b,c).

To help ensure that food value chain development is inclusive,efforts to facilitate connections between smallholders,SMEs,and urban markets should be informed by a good understanding of urbanization patterns. About half the total urban population of developing countries,almost 1.5 billion people,live in cities and towns of 500 000 inhabitants or fewer (FAO 2017). Though often ignored by policymakers,geographically concentrated networks of small cities and towns are the places where rural people market their products,buy their seed and other inputs,send their children to school,and access healthcare and other services. These smaller urban centers can play a key role in accelerating the development of rural economies and making them more inclusive (Christiaensen and Todo 2014;IFAD 2016; FAO 2017).

3.lnclusive value chains:Generating nonfarm and agri-food employment

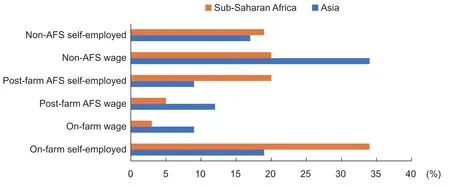

Since agriculture remains the primary source of food and income for the poor in most low-and middle-income countries,stimulating productivity growth among smallholder farmers is one key vehicle for poverty reduction. However,the development of off-farm activity will also be critical.Non-farm employment is already more important in rural low-income contexts than often thought. For example,while 70 to 80% of rural Africans are engaged in own-farming,recent assessments have shown that it accounts for only a third of their employed time (see Fig.4).

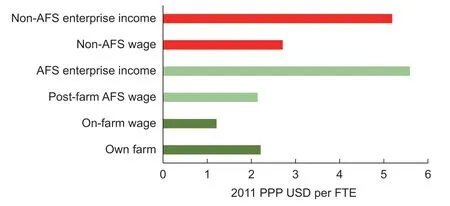

In fact,about 25% of overall rural employment in sub-Saharan Africa and lower-income Asia is in the midstream of food supply chains within wholesale trade,logistics,processing,and retailing. These agri-food system activities are especially important,particularly in terms of income,to women and youth in peri-urban areas and areas beyond.Household survey data for five African countries suggest that rural enterprises’ income (per full-time equivalent) from non-farm agri-food system rural enterprises is more than double the income derived from farm activity and higher than income from non-agrifood system businesses (see Fig.5 based on Dolislageret al.2018).

Development of downstream activities -such as packing fruit and vegetables,collecting,refrigerating,and shipping milk,slaughtering animals and preparing and distributing the meat,and collecting and milling feed grains -thus provides opportunities for inclusive economic development.Urban demand for higher-value,more perishable products provides additional income and employment opportunities for actors along food supply chains. Such products tend to have higher economic value because their proper handling requires activities such as cold storage and transportation,packaging,and processing that tend to be labor-intensive,both on-and off-farm,when operated through SMEs,possibly even more so than the handling of staple foods like grains and pulses (Reardonet al.2019c). The emergence of these activities creates employment multipliers in rural areas and the small towns that service them.

Fig.3 Agrifood sector segments’ shares in GDP in Africa and Asia. Access provided by James Thurlow (IFPRI). Selected countries are ordered in the graph from the lowest (left) to highest (right) GDP per capita (measured in 2011 purchasing power parity(PPP),USD). Source:IFPRI,AgGDP+database.

Fig.4 Employment (full-time equivalent) by occupational categories in on-and off-farm agri-food system (AFS) sectors and non-AFS sectors in sub-Saharan Africa and Asia. Source:authors’ elaboration based on Dolislager et al. (2018). The estimates are based on observed data from recent household surveys in six African countries (Ethiopia,Malawi,Niger,Nigeria,Tanzania,and Uganda) and four lower-income Asian countries (Bangladesh,Cambodia,Indonesia,and Nepal). Dolislager et al. (2018) then used these data to estimate a regression model,which allowed them to project to regional aggregates. Employment shares show weighted averages of the values depicted across all countries.

Fig.5 Wage-earner and self-employed income differentials for on-and off-farm agri-food system (AFS) and non AFS activities in five countries in sub-Saharan Africa. Estimates reflect averages for the five country cases. PPP,purchasing power parity; FTE,full time equivalents. Source:Dolislager et al. (2018),based on LSMS-ISA survey data for Ethiopia,Malawi,Niger,Tanzania,and Uganda,2013–2017.

Agri-food value chains and other rural-urban linkages are the key to unlocking these opportunities. In low-income countries of Africa and South Asia,the rapid expansion of the midstream in food value chains is being driven by the growth and proliferation of SMEs,but has attracted little interest from researchers and policymakers. This “quiet revolution”taking place in food value chains mirrors what happened in other parts of the world in earlier decades (Barrettet al.2019; Reardonet al.2019a,b,c). A wide array of formal and informal SMEs dominates this current phase of food system transformation. Yet weaknesses remain. Tapping the vast potential of food supply chains to drive inclusive transformation will require public policy support to (1)provide adequate infrastructure,(2) create the right market incentives,and (3) facilitate skills development.

3.1.lnvesting in infrastructure and market linkages

Rural infrastructure,including quality rural and feeder roads,reliable electricity,and storage facilities,is essential for propoor growth and improving rural livelihoods. Inadequate rural infrastructure leaves communities isolated,holds back food value chain development,contributes to postharvest food losses,and is significantly associated with poverty and poor nutrition (Shively 2017).

To stimulate farm productivity and raise farm incomes,infrastructure should be designed to help smallholders access markets,and infrastructure investments should align with support measures that help smallholders overcome other barriers,such as lack of access to credit,improved inputs,or land. For small farmers,such investments help smooth income shocks from seasonality,market volatility,and weather variability. For example,in India,cold storage is reducing the seasonality of the potato supply in Delhi and giving farmers in Agra District new marketing options that counterbalance the power of traditional wholesalers(FAO 2017).

A comparative analysis of Europe,Brazil,and Chile suggests that infrastructure investment has the biggest impact on market access when it supports a package for connectivity -including improvements in roads,electricity,and communications technology (FAO 2017). In Brazil,for example,transport times and costs for individual farmers and drivers have been reduced through infrastructure that provides nodes,such as truck stops,for self-organized transportation of products. In Europe,smallholders in the livestock sector have benefited from infrastructure investments that reduce costs to access local abattoirs,wholesale markets,and Internet ordering systems.

Public investment in rural infrastructure can also induce forms of inclusive growth that go beyond linking smallholders to markets. For instance,in southern Chile,investment in rural roads and basic services leveraged significant private investment in the salmon aquaculture industry,which reduced poverty by employing rural women in agrifood industries (Ramírez and Ruben 2015). In central Nicaragua’s milk-producing areas,investments in rural roads,cold storage,and milk processing stimulated strong economic and employment growth that benefited traders and large commercial farmers but did not create direct benefits for poor farmers (Ravnborg and Gomez 2015). And in Nepal,investments in roads and bridges moderated food price levels and price volatility (Shively and Thapa 2017).

Investment needs and potential economic synergies are probably best addressed through a territorial or geographic approach (Gálvez Nogales and Webber 2017; Maruyamaet al.2018). Such approaches include planning of agroindustrial parks,agro-based special zones,incubators,clusters,and agro-corridors,all of which have had varying degrees of success (IFPRI 2019). Infrastructure planning should also support existing “spontaneous clusters” of downstream agri-food businesses,which are too often ignored by national policymakers and donors. Nigeria’s thriving maize feed–chicken system provides a good example of a spontaneous cluster driven by large numbers of SMEs in the midstream (Reardonet al.2019c). To further propel agri-food SME dynamics and facilitate deeper integration of smallholders into markets,policies should promote investments that help strengthen the weakest links,often the supply of electricity,availability of temperaturecontrolled storage,and wholesale market development.

As a result,infrastructure improvements can help dynamize distribution and service networks critical to developing efficient food supply chains and generating a vast source of off-farm employment. In this way,infrastructure forges spontaneous SME clusters that will further reduce transaction costs for smallholder farmers -directly by connecting them to markets and indirectly by reducing transaction costs for wholesalers (who supply raw inputs to processors). Logistics clusters or hubs such as truck stops tend to emerge near both wholesale markets and SME processors,further reducing the cost of market linkages.This is the case,for example,with the clusters of maize milling SMEs in Dar es Salaam and Arusha,located near wholesale grain markets,and for first-stage processors and milk collection centers in rural Zambia,some of which are SMEs (Nevenet al.2017; Snyder 2018).

3.2.Price incentives and food quality regulation

In addition to infrastructure,adequate price incentives are critical to facilitate greater inclusion of small farms and businesses in sharing food system value added,especially price policies that help reduce the level and variability of energy costs. Food processors and distributors rely on consistent,affordable access to electricity. In addition,because much of the equipment used in agri-food businesses in Africa and South Asia are imported,low tariffs facilitate rapid development of food supply chains and job creation.

Helping farmers meet higher food quality standards through regulation and quality certification can also improve market access and incomes for small farmers,making food systems more inclusive. Governments are responsible for protecting consumers,SMEs,and individuals from substandard products,whether poor quality seeds and fertilizers or damaged or contaminated food products.Quality certification can also help protect farm-level investments,expand the use of quality seed and fertilizer,increase output,increase SMEs’ competitiveness in regional and global markets,and protect consumers. Supermarkets set high standards for quality,safety,and consistency,thereby placing new demands on farmers. For example,food safety concerns become an issue when demand increases for milk,meat,fish,vegetables,edible oil,peanut butter,other similar products,processed food,and food prepared in restaurants.

As large firms take a bigger share of the overall processing sector,SMEs and smallholders will likely face growing challenges in meeting the private standards set by supermarkets and large processors. Meeting these standards will require various “threshold investments” in food safety,quality,volume,and consistency by small-scale farmers,which may be cost-prohibitive to asset-poor farmers(Barrettet al.2019; Reardonet al.2019b,c). In response,governments should consider assisting smaller farms and agri-food operators lacking the means to comply with such initial requirements.

3.3.Promoting skills and entrepreneurship training

Fostering rural entrepreneurship and employment diversification,especially for women and youth,requires developing general skills,such as running a business,accessing market information,and using information and communications technologies (ICTs). A more skilled labor force in low-income countries would increase agricultural productivity and stimulate the growth of high-productivity services and industrial sectors and enjoy access to betterpaid jobs. Policies supporting education at all levels are important to inclusive rural transformation,although their impacts are felt only in the long term. Measures to increase the employability of rural youth include strengthening vocational training and basic education,establishing mechanisms for recognizing informal-sector work experience,and creating greater awareness of job opportunities and labor rights.

However,agri-food businesses in Africa seem to see technical labor skills as less of a constraint on growth than high energy costs and inadequate roads (Arslanet al.2019).Further,most firms consider improved basic education and training in social,organizational,and entrepreneurial skills more important than general technical training. In terms of specific technical skills,proficiency in or knowledge of digital technologies,processing techniques,food safety,and ICT-enabled commercial procedures are the most needed.

3.4.lmproving vehicles for financial inclusion and expanding business development services

Inclusive agribusiness models will also revolve around access to credit for both smallholders and SMEs in the middle segments of the food value chain and ancillary services they may need. In this respect,dedicated financial facilities and investment vehicles are increasingly being used to support farmers and agribusiness as part of agroterritorial development. For example,the Beira Agricultural Growth Corridor initiative in Mozambique envisioned three types of financial facilities for companies and farmers in the corridor:working capital to support agricultural production,social venture capital to promote pioneer investments,and long-term capital for agriculture-supporting infrastructure within the corridor (FAO 2017).

Agri-territorial approaches can be instrumental in enabling the flourishing of SMEs in the agri-food sector. In China,agro-industrial parks have helped small-scale park tenants to grow into medium-sized and large enterprises (Dinhet al.2012). India has promoted food parks that improve SMEs’access to cold storage,quality control laboratories,and warehouses. Parks also create scope for joint purchasing that reduces the cost of inputs,allowing participating SMEs to scale up within a short time generating income increases for all operators along the food supply chain (Gálvez Nogales and Webber 2017).

4.lnclusive value chains:connecting smallholders to markets

The “quiet revolution” in the downstream of food supply chains is also changing farming systems. Growing demand for higher-value food products means that farmers must change the crop production mix. New efficiency requirements and policies have encouraged mechanization and the adoption of modern inputs. However,smallholders have often been left behind because they lack the resources needed to adapt to the changing food system.

Initiating and sustaining a process of inclusive transformation requires market access and other supports for smallholders to trigger sustainable productivity growth and foster their remunerative participation in food value chains (Poultonet al.2006; Barrett 2008; Reardon and Timmer 2012). Here we focus on four instruments for promoting the inclusion of smallholders in agri-food supply chains:(1) securing land tenure; (2) leveraging the potential of digital technology for smallholders; (3) promoting inclusive agribusiness models; and (4) enhancing the capacity of farmers and other food chain actors to manage and cope with risks.

4.1.Land tenure policies for productivity growth and inclusive value chain development

Secure land tenure can stimulate agricultural development and improve the well-being of landholders by improving access to credit and input markets and facilitating land rental and sales markets. Securing land tenure can increase farm productivity,raise farmers’ incomes with limited land,and even facilitate the transition to off-farm activities (Deiningeret al.2014,2017). Secure land tenure has,for example,been found to improve productivity in Madagascar,provide incentives to farm-level investment in West Africa,and enhance market access in Chad (Fenske 2011; Bellemare 2013; Corsiet al.2017). In many contexts,securing these rights for women can be especially difficult,creating obstacles to gaining access to credit and inputs,requiring a gender-sensitive approach to the design of land tenure policies and instruments for smallholders (Meinzen-Dicket al.2019).

Land tenure plays a role in overcoming hurdles posed by excessive fragmentation of landholdings. An estimated 84%of the world’s farms are smaller than 2 hectares. In many low-and lower-middle-income countries of Africa and South Asia,average farm size is shrinking,to the point that many farm units using traditional farming practices are no longer economically viable (Lowderet al.2019). At the same time,investors are consolidating farmland,and the number of medium-sized farms is increasing in high-potential areas. As mentioned earlier,while small farms’ land productivity tends to be relatively high,their labor productivity tends to be low because smallholders lack the necessary scale to access markets or adopt new technologies (underscoring the importance of public rural services and farmers’ collective actions,discussed below). Development of efficient land sale and rental markets,which depend on secure property rights,can give farmers access to larger plots that help them achieve economies of scale. Recent evidence suggests that land rental markets are more common than previously thought. For example,in Bangladesh and Togo,40% of holdings are rented or operated under systems other than farmer-owned tenure (Lowder and Bertini 2017).

Secure land tenure also supports the development of rental markets for equipment such as tractors and the use of improved seeds and other inputs. Agricultural mechanization is critical to boosting productivity because it enhances the performance of other inputs. Mechanization has increased worldwide,especially in those countries that have undergone a rapid transformation,and has proved profitable for small-scale farmers. For small farms,equipment rentals and shared use through farmer cooperatives can enable successful mechanization,as has been the case in parts of East Asia,where use of farm machinery facilitated by rental markets has increased sevenfold since 1985 (FAO 2017).

Secure land tenure may also increase smallholders’access to water,as it provides incentives to farmers to make long-term investments in both land and water management.However,research on land policies in Ethiopia and Ghana suggests that policies to strengthen land ownership or usage rights on their own may be inadequate and need supplementary support measures (WLE 2017).

4.2.Leveraging the potential of information and communications technology

Face-to-face extension services and farmers’ relationships with buyers are increasingly complemented -and sometimes replaced -by information channeled through modern ICTs. This is bringing new benefits to smallholders.In India,for example,Internet service provided by a private food conglomerate to rural areas has given farmers access to more information,empowering them in the negotiation of farmgate prices (FAO 2017).

Mobile phones,in particular,are increasing farmers’access to information. Mobile phone coverage and adoption have significantly increased in developing countries over the past two decades. In Africa,coverage has expanded from less than 10% of the population in 1999 to more than 90%today. In terms of actual subscribers,45% of Africans now have mobile phone access,and 50% are expected to by 2025. In Asia,66% had phone access in 2019,and 72%are expected to by 2025 (GSMA 2019).

Mobile phones effectively shorten the distance between isolated smallholders and other actors involved in processing,transporting,marketing,and regulating farm produce (Conway 2016). ICT connectivity allows farmers to seek solutions from peers and expands access to a range of other information sources. For instance,Sri Lanka’s FarmerNet,a virtual trading floor,connects traders and farmersviatext messaging (FAO and ITU 2016). Mobile phones have sped up input delivery through e-vouchers and real-time inventory tracking. As another example,Nigeria introduced an e-wallet program that directly delivers seed and fertilizer vouchers to farmers’ phones. The platform has been extended to deliver other benefits,such as vouchers for nutritional supplements (Adesina 2016). In Kenya,the Kilimo Salama (“safe agriculture”) pilot program uses weather stations to detect excessive and inadequate rainfall.It sends a payment to affected farmers through M-Pesa,a mobile money transfer service (FAO and ITU 2016). ICTs can also make local access to credit and rural advisory services timelier and more efficient. Finally,it is hoped that ICT-savvy young people in Africa and South Asia will be able to seize new employment opportunities emanating from the widespread deployment of these technologies in agri-food systems (Mabiso and Benfica 2019).

4.3.Promoting inclusive agribusiness models

Producer organizations and inclusive forms of contract farming help smallholders overcome constraints to economies of scale and strengthen their access to markets.For instance,producer organizations allow small farmers to engage in collective marketing,reducing their transaction costs,allowing them to share risks,and improving their bargaining power. These organizations link farmers to upstream and downstream actors,thereby helping farmers to obtain better terms,for example,through fairer contract farming schemes (Prowse 2008). Acting collectively in associations also enables farmers to comply with food quantity,quality,and delivery requirements in supermarket contracts (Herbelet al.2012). Small-scale vegetable producers’ groups in Kenya,for example,can meet modern market requirements. The country’s banana and mango producers have also benefited from participating in collective marketing schemes. However,among Kenya’s mango producers,medium-scale mango farmers benefit more than small-scale farmers from shared marketing (Mutonyi 2019). In contrast,in China,small-scale farms generally benefit more than medium and large farms,highlighting the importance of context (Liuet al.2019).

Producer organizations also facilitate access to credit,directly by managing microcredit systems and indirectly through innovative arrangements such as warehousereceipt systems,in which stored produce is used as collateral to obtain short-term loans. Because producer organizations can help farmers meet their financial needs and overcome liquidity constraints,they are especially attractive to smallholders (Berdeguéet al.2011).

Support for small farmers is particularly important today as global input markets consolidate,giving agribusiness input and technology providers little incentive to invest in small farms in developing countries. This context underscores the need for policy interventions that address market failures and respond to small farmers’ needs,especially through the provision of public goods such as rural advisory services and support to farmers’ collective action.

4.4.Social protection for risk management and local economic development

For instance,social protection in the form of food aid or cash transfers is crucial to smallholders’ risk management during rural transformation and for building resilient rural livelihoods. Social protection allows poor rural households to invest in riskier but more-remunerative livelihood activities.Essentially,these transfers can affect investment decisionsviathree pathways:(1) managing risks,(2) relaxing liquidity,credit,and savings constraints,and (3) generating spillover effects into the community and local economy (Alderman and Yemtsov 2014; FAO 2015a; Tirivayiet al.2016).

In a recent positive trend,social protection programs link social transfers to promoting rural employment and agricultural production. In Lesotho,a cash transfer program had a larger positive impact on agricultural production when combined with a program to improve homestead gardening (Daidoneet al.2017). Other programs link public food-purchase schemes and school-feeding programs to smallholder family farmers as suppliers. A recent study found that a home-grown school-feeding program in 10 regions of Ghana had positive impacts when mechanisms were in place to enable smallholders’ participation and ensure access to input support services (Gelliet al.2016).Impacts tended to be greater for context-appropriate food items -those that are agro-ecologically suitable and financially viable for small-scale production (Singh and Fernandes 2018).

Ethiopia’s Productive Safety Net Program (PSNP) is another example with generally positive impacts. The PSNP provides chronically food-insecure rural households with a combination of cash or food transfers (direct support),and transfers through the contribution of labor to public works or livelihood development or both. Impact assessments that compared PSNP and non-PSNP households found that both public works and livelihood support programs have had a significant positive impact on participation in non-farm business activity (Gilliganet al.2009; Tadesse 2018). On average,the programs increased the probability of engaging in non-farm activities (mostly in downstream food supply chain activity) by 5 to 7 percentage points.Related assessments found that the program also positively impacted crop yields and the broader development of the local economy,without creating adverse incentives for agricultural producers (Filipskiet al.2016; Arega and Shively 2019).

5.Conclusion and policy recommendations

The potential to create new jobs and better incomes by strengthening food system linkages is substantial,given the growth of food markets propelled by urbanization,income growth,and related changes in dietary patterns. These changes provide opportunities for significant growth in rural incomes and improvements in smallholder livelihoods,as well-integrated networks of downstream activity develop with new requirements for high-value-added food items,food quality,and food safety. COVID-19 is causing enormous setbacks in global poverty reduction and the eradication of hunger. In most countries,the current (July 2020) policy focuses on containing the spread of the pandemic,among other things,through social distancing measures and emergency responses to mitigate the economic impacts. It is imperative that food sectors are considered essential,as is the case in most contexts,to avoid major disruptions in food supply chains and human devastation from inadequate access to food. Poorer nations are feeling the repercussions of the economic fallout in major affected countries,limiting import capacity and further constraining fiscal capacity to soften these indirect impacts of COVID-19 on their populations’ incomes and livelihoods. Emergency economic relief efforts are thus essential to prevent this health crisis from becoming a food crisis. Having said this,the discussion in this paper also made clear that inclusive,resilient,and well-functioning food supply chains are essential in providing remunerative and stable livelihoods to most of the world’s poor and vulnerable. This holds all the more in the post-COVID-19 era. Also,there is no reason to believe that food sector growth and transformation will not continue following the recovery from COVID-19. Hence,it will be essential to accompany emergency responses with long-term support measures as outlined in this paper to leverage inclusive transformations of food systems in developing countries and secure resilience to future pandemics and other shocks.

This approach should nourish the ongoing “quiet revolution” that integrates and modernizes food value chains in Africa and South Asia and makes sure the millions of SMEs in the “hidden middle” do not perish under the weight of COVID-19 restrictions the global economic recession. Long-term policies subsequently can guide this transformation process to ensure that the economic gains from an expanding agri-food sector are shared fairly among supply chain actors,beginning with smallholders,and help address rural needs in regions with the greatest poverty pressures and employment needs. In this regard,this paper has provided a range of policy options and instruments that may help make food systems more inclusive for smallholders and rural populations. None of these is a silver bullet,however. Typically,combinations of interventions will be needed to provide the enabling environment for market actors to invest in and innovate to develop well-integrated food supply chains. To help smallholders connect to markets and help off-farm job creation flourish,policymakers will need to look across the food system to identify and address the weak links.

Such a food system approach will also be needed to align the objective of developing more inclusive food supply chains with other key food system objectives. Our discussion has already underscored the potential trade-off between moving toward an enhanced,consumer-focused food safety regulatory environment and ensuring the financial viability of small farms and food businesses. Other such trade-offs concern possible increases in the ecological footprint of longer supply chains and the non-communicable disease risks associated with the “Westernization” of diets(notably excess intake of salty and sugary processed foods and animal-sourced foods).

To effectively balance such trade-offs,policymakers and analysts will need much better data. At present,policymakers are largely flying blind when it comes to the broader food system. We lack adequate statistics to depict the entire food chain from farm to fork. Farm and household survey data do provide insights into farming systems and farm household income generation as well as food consumption and nutritional outcomes. But the data from enterprise,market,and field surveys necessary to understand the relative importance and functioning of other parts of the food system,especially those in the midstream,either do not exist or are scattered or buried among different sources. This “hidden middle” extends both to large public assets like domestic wholesale markets and to small private operations,including the millions of food traders and logistics,processors,and service providers.

This data gap hinders policy research and,hence,policy guidance. Governments must invest in improved data gathering to provide policymakers with the evidence they need to craft policies that effectively support and promote inclusive value chains across the entire food system.

Acknowledgements

This research was supported by the Consultative Group on International Agricultural Research (CGIAR) research program on Policies,Institutions and Markets (PIM) and Food and Agriculture Organization of the United Nations.

Declaration of competing interest

The authors declare that they have no conflict of interest.

杂志排行

Journal of Integrative Agriculture的其它文章

- Paths out of poverty

- The power of informal institutions:The impact of clan culture on the depression of the elderly in rural China

- Does empowering women benefit poverty reduction? Evidence from a multi-component program in the lnner Mongolia Autonomous Region of China

- Status and path of intergenerational transmission of poverty in rural China:A human capital investment perspective

- The impact of the New Rural Cooperative Medical Scheme on the“health poverty alleviation” of rural households in China

- The effects of social security expenditure on reducing income inequality and rural poverty in China