The Outlook for China's Trade Finance Development

2018-06-19ByXuJun

By Xu Jun

Trade finance practitioners are facing a new and complex mix of challenges.

C hina's trade finance business has made significant strides in recent years,resulting in a major contribution to global trade. However, trade finance practitioners are facing a new and complex mix of challenges amid a slowing economy, tougher regulatory requirements, trade protectionism and a growing pushback against globalization.

From 1953 to 1993, Bank of China was designated as the state's specialized foreign exchange bank, exclusively handling the nation's settlement and financing of foreign trade. Since the reform of foreign exchange management system in 1994, all commercial banks with a foreign exchange business license have been permitted to conduct foreign trade finance business.

However, according to statistics collected by the International Chamber of Commerce China, even though many newly established local municipal and rural banks have begun trade finance operations, the business has largely been concentrated in stateowned commercial banks, policy banks and medium or large shareholding commercial banks.

Trade banks account settlement transactions on about 70% of the country's global trade in goods, and these banks have been used as samples for data analysis in this study.

In China, the trade finance business covers a wide range of products and services, including trade settlement (or payment) products (LCs, documentary collection and cross-border remittances),trade-related financing products, and bank guarantee/standby LCs among others.

Unlike in the West where banks typically do not include cross-border remittances as trade settlement products,trade finance departments in most banks in China are responsible for all of the abovementioned trade finance businesses and supply chain finance. According to a survey covering 62 banks, trade finance departments in 58 banks manage international remittance business in addition to LCs, documentary collection,guarantee/standby LCs and trade-related finance. In a handful of banks, the trade department manages international trade transactions exclusively.

Recently, in order to provide comprehensive and seamless financial services to their clients, more banks have been considering organizational reform from traditional trade department to transaction banking by integrating their transaction-related financial sectors.

Fintech

With the rapid development of e-commerce in China, banks are employing an array of measures to meet customer demand, comply with internal control requirements and compete with e-commerce providers.These measures include trade financerelated digitization and fintech research and practice, including eUCP(uniform customs and practices),eURC (a supplement to the Uniform Rules for Collections for Electronic Presentation), e-supply chain finance,e-guarantees, and blockchain domestic LCs, factoring and forfeiting.

Trade Settlement Trends

Major trade banks in China established trade processing centers about a decade ago, and the scope of business has varied. For example,some banks centralize the importrelated payment procedures and bank guarantee/standby letters of credit,while others centralize all trade finance products.

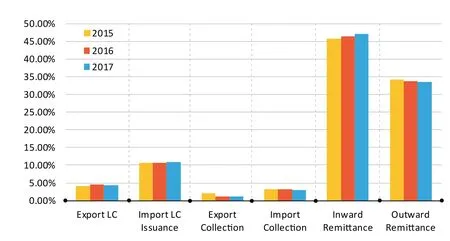

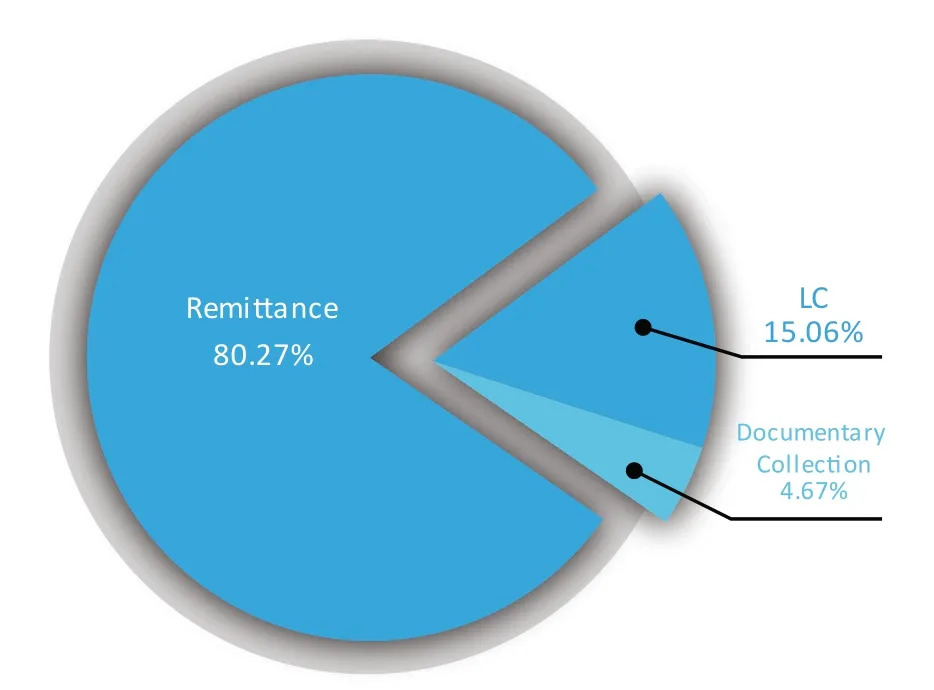

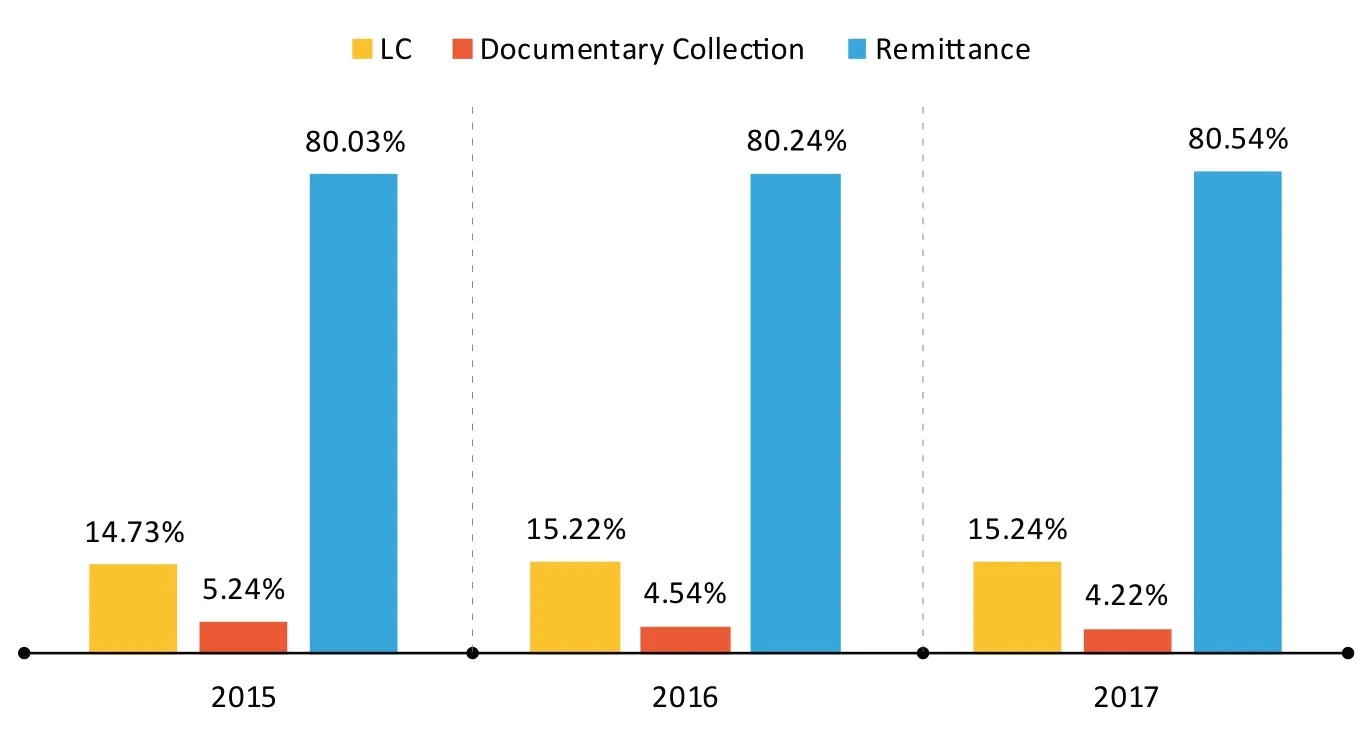

Prior to 1994, LCs were the dominant payment method in international trade.However, with the rapid development of China as a trading power, crossborder remittances have been on the rise,accounting for 80.27% of payments in value terms between 2015 and 2017. LCs were 15.06%, a decrease from 18.55% in 2014, though there was a modest upturn in 2015. The data also reveal the usage of LCs generally rises in times of global economic slowdown.

However, the percentage varies in terms of payment methods in different part of the country. For example, in 2017, in one developed province where importers and exporters are generally major corporations, the average percentage of remittances reached 90.52% of total transaction value, while LCs accounted for only 6.81%. In the same province, one city with a high concentration of original equipment manufacturers recorded only 3.81% of its global transactions using LCs, while remittances took an overwhelming 93.88% share.

It can be seen that in export trade transactions, inward remittances have increased by about 1 percentage point per year as a proportion of total cross-border payments since 2015,with an average percentage of about 46.43%, while the average percentage of export LCs was 4.32% and export documentary collection was 1.5%.

Unlike export trade transactions,there is a different picture for import payments. Outward remittances were 33.84% of all transactions, 12.59 percentage points below the figure for inward remittances. The average percentage of import LCs was 10.74%,6.42 percentage points higher than export LCs. Import collection was 3.17%, 1.67 percentage points higher than that of export collection.

Key Reasons for Payment Differences

The basic reasons for the difference between import and export trade transactions when using remittance as a payment method may reflect the following factors:

China is one of the largest members in the global supply chain,but the bargaining power of exporters(especially small and medium enterprises) with big overseas buyers is comparatively weak. Buyers are usually reluctant to use LCs due to the higher costs and complicated procedures.Remittances, however, offer greater convenience and cut costs.

Since China launched its reform and opening policy in 1978, major exporters have established long term relationships with their counterparties,and LCs have lost ground as the preferred vehicle for protection against credit risk. More and more exporters are using export credit insurance as the risk mediation measure against buyers'credit risks when using remittances.

LCs are not popular with large exporters when trading with buyers of good credit standing due to their complicated procedures, heavy paperwork and prolonged time for the receipt of accounts receivable. Small and medium size exporters tend to use remittances much more frequently as well. On one hand, SME bargaining power is weak, as stated above. On the other hand, many SMEs are not familiar with LCs and do not treat them as a safe payment method because of frequent refusals.

The difference in the use of import LCs and export LCs may be related to the fact that China is one of the largest commodity merchandise importing countries. LCs are commonly used in commodity trade transactions due to the special procedures and traditional trade finance structures.

Two Sides of the Coin

According to a rough estimate from several banks, there is a big difference between the refusal rate under export LCs (about 30%) and import LCs (about 1%).

There are at least two reasons for the low rate of import LC refusals.For one, the Supreme People's Court promulgated the Provisions of the Supreme People's Court on Some Issues in the Adjudication of Letter of Credit Related Cases in 2005, and issuing banks in China have been more cautious in raising discrepancies ever since. Banks in China are also paying more attention to their international creditworthiness and more experienced LC practitioners are available.

However, almost all the banks surveyed in China have described confirming banks as being extremely exacting resulting in high rates of refusals (about 90%). That may contribute to fears that the confirming bank could be rejected by the issuing bank.

Trade Finance Trends

In the past, most trade finance products were provided to customers on an LC or documentary collection basis. However, with the increasing use of remittances, LC or collection-based trade finance business volumes have been decreasing and remittance-based trade finance business volume have increased accordingly.

The only exception to traditional trade finance product is the bank guarantee/standby LC which has seen a significant increase in use.International Chamber of Commerce rules are more acceptable in guarantee business in China. International guarantees issued subject to URDG758 are increasing (even some domesticrenminbi guarantees are subject to Uniform Rules for Demand Guarantee 758), while standby LCs are subject to International Standby Practices 98(which used to be subject to UCP600)have seen an increase. The Supreme People's Court of China promulgated the Supreme People's Court Decision on Some Issues in the Adjudication of Independent Guarantee Related Case in 2016, and has encouraged the use of independent domestic and overseas guarantees.

Table 1: Average percentage of payment methods in China from 2015 to 2017

Table 2: Percentage of payment methods in China from 2015 to 2017

Table 3: Breakdown of payment methods in China from 2015 to 2017

Rapid Development of Supply Chain Finance

According to Qian Zhan Industry Research Institute's supply chain finance (SCF) industry report in 2014,the scale of supply chain finance may reach about US$2.3 trillion.Mainland China started applying the SCF technique from the factoring business in 1987. This developed quickly after 2000 along with the transition of payment methods from LC or documentary collection to remittances (open account). According to the Finance Competitiveness and Innovation Global Practice report,China went through 15 years of uninterrupted high growth in factoring,and surpassed the United Kingdom as the largest factoring market in the world in 2011.

The initial use of supply chain finance was in 2006. Despite the fact that most banks are not familiar with Standard Definitions for Techniques of Supply Chain Finance, almost all of the techniques mentioned are used by SCF providers,though in different names. It appears that banks and other non-bank SCF providers welcome the standard definitions.

On October 5, 2017, China's State Council published the State Council's Guidance on Actively Promoting Supply Chain Innovation, which calls for the promotion of supply chain financing to serve the real economy. It encourages commercial banks and other anchor parties of the supply chain to set up SCF platforms and provide efficient and simplified financing channels to SMEs.It also encourages the development of online SCF services, including account receivables finance. SCF will definitely see a significant increase as a result of this government effort.

Challenges for Trade Finance

The government has set up its strict compliance policy on financial institutions from last year with full range for supervision from anti-money laundry, anti-financial crime regulations,"know your customer" requirements,true trade background screening, and the entry of trade finance products in credit-related management and operations. At the beginning of this year, regulatory authorities in China issued a series of policies strengthening their supervisory measures, and banks will be severely penalized for violating regulatory requirements.

Since 2004, the People's Bank of China(PBOC) has issued its annual Anti-Money Laundering Report. According to its 2016 report, the PBOC worked with the Financial Action Task Force and the World Bank on anti-money laundering efforts and anti-terrorism financing policies and evaluation. In 2016, the PBOC conducted special anti-money laundering inspections of 955 banks and penalized 155 banks for violations of anti-money laundering laws and regulations.

In the effort to meet regulatory requirements and internal policies, banks have been facing difficulties in know your client due diligence investigations due to the lack of sufficient measures. The fact that different banks adopt different standards complicates the situation. The processing speed is greatly influenced and prolonged from one or two days to several days, or even several months for know your customer and transaction background verification purposes.

SMEs are among the most vulnerable customers who are often unable to provide the necessary information of their counter trading partners (e.g. shareholders). Local medium to small sized banks are also among the most affected ones due to the termination of correspondent banking relationships by overseas banks.

Capital Treatment, Credit Policies and Pricing

With the enforcement of Basel III and new accounting principles IFRS9,the fact it that capital treatment, credit policies, and pricing are all presenting challenges to the trade finance businesses all over the world. China is no exception.

In recent years, with the increasing pressure of capital requirements, banks are focusing on developing trade finance products which may give more flexibility in avoiding capital constraints, for example,forfaiting, especially secondary forfaiting market. According to the International Trade and Forfaiting Association contribution in the International Chamber of Commerce Rethinking Trade & Finance 2017, the forfaiting market in China stands at about US$30 billion. Forfaiting is a very good channel for SMEs to get access to trade finance.

Pricing for most of trade related finance products is not more competitive than that of working capital as well at the same time in almost all banks in China. This in turn adds to the difficulty in promoting traderelated finance products.

In the past few years, due to defaults of some major corporations and a considerable number of SMES and some significant fraud cases in trade, banks in China have adopted more stringent credit criteria, and access to credit facilities(including trade finance) is becoming more difficult.

Outlook for Trade Finance in China

It is obvious that trade banks in China are facing profits issues with payment methods change, compliance pressure, capital requirements,correspondent relationships, and trade protectionism. Challenges also exist as some of the trade settlement products such as LCs are labor intensive and costly.

However, trade finance products and payments are recovering from a decline over the previous three years.

The Chinese government's efforts in supporting globalization, trade facilitation under the Belt and Road Initiative (a major trade and investment strategy), and easier access for SMEs to affordable finance have provided a solid base for the development of trade finance business. It is believed that cross-border guarantees will continue to increase especially with the promotion of the Belt and Road program not only for banks in China, but also for those in regions or countries covered by the initiative.

Banks' internal transformation as a result of organizational reform, strategic adjustments, or a focus on fintech development may help trade finance rise to new levels.

The author is deputy general manager of global trade services at Bank of China's Jiangsu Branch