International Capital Flows and China's Bond Market

2018-06-19ByXieYaxuan

By Xie Yaxuan

China's bond market will show net inflows of international capital through the first half of 2019, but on a markedly smaller scale.

C hina's domestic bond market saw a surge of international capital inflows in the first half of 2018. What was behind this sharp increase? What was the impact on longer term interest rates and the renminbi's exchange rate? And will the upward trend continue? The following article seeks to examine these questions.

Data from three different organizations show that in the first half of 2018, international investors substantially increased their holdings of Chinese bond assets. The State Administration of Foreign Exchange (SAFE) said in its China's Balance of Payments publication that investments in Chinese bonds from overseas reached a net US$75.7 billion in the first half of 2018, up 741% from a year ago. US$69.8 billion of that total came from overseas institutional investors. In the same period, Chinese domestic renminbi financial assets held by overseas institutions and individuals were valued at 404.1 billion yuan, up 923% year on year,according to the People's Bank of China publication Domestic RMB Financial Assets Held by Overseas Entities.Statistics from the China Central Depository & Clearing Co.Ltd. and Shanghai Clearing House showed that the balance of Chinese domestic bonds held in trust by overseas institutions reached 400.9 billion yuan at the end of the first half of 2018, a year-on-year growth of 969%.

Factors Behind the Investment Upturn

The large increase in international investment reflected cyclical and structural factors.

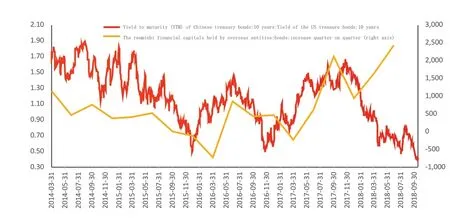

There are two cyclical factors that influence investment enthusiasm for Chinese bond assets. The first is the spread between yields on US treasury bonds and Chinese government debt. Chinese treasury bond yields are matched against US treasury bonds with the difference as the opportunity cost. In this case the difference between the yields serves as a bellwether for overseas investment in the Chinese bond market(See Chart 1). The difference between the 10-year Chinese and US treasury bond yields slipped from as much as 180 basis points in 2014 to as low as about 40 basis points at the beginning of 2016. After the decline in yield spreads,international investment in Chinese bonds declined,reversing the 2014 third quarter's net purchases of 74.8 billion yuan to net sales of 71.7 billion yuan in 2016.

In contrast, purchases by foreign investors rose when the spreads between Chinese and US treasury bond yields recovered from their lows.Spreads widened from about 55 basis points in the fourth quarter of 2016 to 160 basis points by the end of 2017.This reversed net sales of 22.4 billion yuan in the first quarter of 2017 to net purchases of 212 billion yuan in the third quarter and 94.6 billion yuan in the fourth quarter of the same year. Investor enthusiasm has increased in 2018, despite the narrowing of spreads from a high of 160 basis points to about 60 basis points in the second quarter.

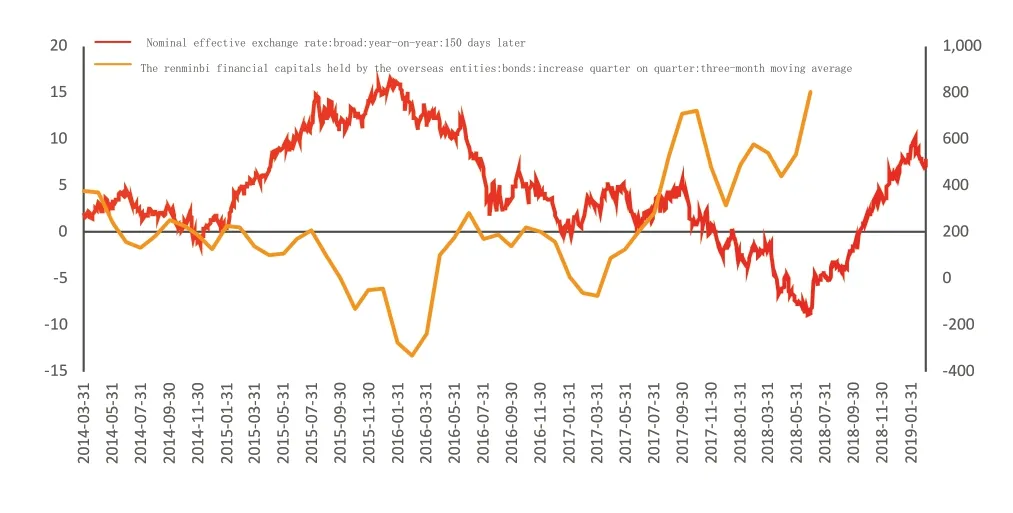

The second factor is the effective exchange rate of the US dollar. There is a negative correlation between a strong US dollar and dollardenominated cross-border bank loans. That is, when the US dollar strengthens against the currency of another economy, capital flows out of that country; when the US dollar is weak, capital flows in. The negative correlation is apparent in international investment in Chinese bonds,but there's a time lag of three to six months. As shown in Chart 2, international investment in Chinese bonds shows up five months after a change in the effective US dollar exchange rate. The fall in the effective rate from the high levels of the third quarter of 2015 has been an important cyclical factor driving purchases of Chinese bond assets by international investors since the second quarter of 2016.

Chart 1: The difference beween yields of Chinese and US treasury bodons - a key factor in international investment interest

Chart 2: The decline in the effective exchange rate of the US dollar has driven international capital into emerging markets

There are two key structural factors affecting international investment in the Chinese bond market. First,it is worth considering how open the domestic market is.China has been proactively expanding the openness of its market to foreign capital and enhancing convenience for bond market investors. Since 2016, a number of measures have been put in place. For example, in February 2016,qualified foreign financial institutions were allowed to invest in China's inter-bank bond market without any limits on the size of their investments, as per the central bank's Circular on Further Improving the Investment in the Interbank Bond Market by Foreign Institutional Investors (PBOC Document No. 3 2016). "Qualified foreign financial institutions" are those identified by the central bank as medium- or longterm investors, including commercial banks, mutual funds,pension funds, insurance companies and charities. In May 2016, the Regulations on Investment in the Interbank Bond Market by Overseas Institutional Investors (SAFE Document No. 12 2016) allowed overseas institutional investors to remit funds related to investments in the interbank bond market in or out of the Chinese mainland as long as these fund movements complied with foreign exchange regulations.

In February 2017, the SAFE Circular on Foreign Exchange Risk Management for Foreign Institutional Investors in the Interbank Bond Market(SAFE document No. 5 2017)provided foreign institutional investors with a way to access the interbank foreign exchange derivatives market on the mainland. Investors have been able to hedge against the risk of exchange rate by selling and buying foreign exchange products such as forwards, swaps and options. Further to these announcements, in May 2017,the PBOC and the Hong Kong Monetary Authority jointly announced a plan to launch the Bond Connect Program.The following month, the PBOC released its Interim Measures for Administration of Mutual Access and Connection between Mainland and Hong Kong Bond Markets.In July of the same year,the Bond Connect program was officially launched. In addition, measures such as tax relief and the introduction of foreign credit rating companies into the bond market have been taken to facilitate foreign investment and enhance China's attractiveness. In March 2018,Bloomberg announced that,starting from April 2019,renminbi-denominated China treasury bonds and policy bank bonds would be included in the Bloomberg Barclays Global Composite Index. This was to be completed over a period of 20 months.

Another factor has been the internationalization of the renminbi. The steady expansion of the renminbi's international role will help attract more foreign investors to the Chinese bond market. Foreign exchange reserves held in renminbi by other countries are a case in point. In the first half of 2018,other economies increased their holdings of renminbi as foreign reserves. The total rose 69.9 billion yuan, up 660% from the 9.2 billion yuan in the same period in 2017, according to statistics from the International Monetary Fund. (The IMF has been disclosing such figures since December 2016 following the inclusion of the Chinese currency in the Special Drawing Rights.) Those national governments holding renminbi generally chose Chinese treasury bonds as a way to ensure the security and liquidity of their reserve assets. Therefore,changes in the foreign exchange reserve assets held by other economies are closely related to changes in the balance of Chinese Treasury bonds.

Although structural factors such as renminbi internationalization can explain some of the increase in purchases of Chinese bonds by international investors in the first half of 2018, this does not mean that cyclical factors such as market expectations were not important.

Lower Bond Yields,Greater Volatility

Chart 3 International investment in the Chinese bond market depressed long-term bond yields

Chart 4 The effect of capital flows on the renminbi's effective exchange rate

Many economists,including former US Fed chairman Alan Greenspan,maintain that the continued increase in holdings of US treasury bonds by foreign investors is an important factor in the continued decline in US long-term bond yields. According to an estimate by the Federal Reserve, if purchases of US treasury bonds by foreign governments are reduced by US$100 billion a month, the interest rate on US five-year bonds will rise by 40-60 basis points.

The impact of treasury bond purchases on bond yields also can be seen in emerging economies. A working paper by the International Monetary Fund in 2014 based on data from 12 countries (Brazil, the Czech Republic, Hungary, Indonesia,Korea, Malaysia, Mexico, Poland, Slovenia, South Africa,Thailand and Turkey) shows that in these emerging economies,a rise in the share of foreign holdings in a country's domestic currency bond market will depress bond yields and increase volatility. Since the subprime mortgage crisis, an increase of one percentage point in the proportion of foreign investors in emerging economies has resulted in a 7-9 basis point decline in the yield of domestic treasury bonds.

It is estimated that as of the end of August 2018, the proportion of international holdings in the Chinese treasury bond market rose to 8% from 5% at the end of the previous year. That resulted in a decline in a 21 to 27 basis point decline in China's 10-year treasury bond yield. Although international inflows into the Chinese bond market had been relatively stable for quite some time, there has been more volatility in recent years. If we accept the fact that the flow of foreign capital has a significant impact on China's longterm bond yields, then we need to deal with the fact that the volatility of long-term bond yields will inevitably increase.

Effective Exchange Rate and Volatility

If other factors remain unchanged, the international capital inflows attracted to the bond market will change the supply and demand situation on the foreign exchange market,increasing the supply of foreign exchange and pushing up the renminbi exchange rate. Between July 2017 and June 2018, large volumes of international funds flowed into the Chinese bond market.According to international balance of payments data,there was a net inflow of US$149.6 billion over the 12-month period, compared with a net outflow of US$21.2 billion from July 2015 to June 2016 and a net inflow of US$37 billion between July 2016 and June 2017. This was one of the main reasons for the 5.4% rise in the renminbi's effective exchange rate over this period.

However, it is essential that we keep in mind that international capital also flows outwards at times. After the opening up of the capital market, the two-way flows of international capital will result in significantly increased volatility of the renminbi exchange rate.

International Investment Trends

From the above analysis,it can be seen that from the second half of 2017 through the first half of 2018, both cyclical factors and structural factors were conducive to bringing international capital into the Chinese bond market.However, looking at the trends in the second half of 2018, the structural factors of a continued opening-up of the domestic market and the internationalization of the renminbi have supported inflows, but cyclical factors have turned negative.

Rising US Bond Yields

In early October, the 10-year US treasury yield rose to 3.23%, its highest level since mid-2011. The rise mainly resulted from three factors.The first was tighter monetary policy in developed countries.In the US, the Federal Reserve continued to raise interest rates and unwind assets on its books. Meanwhile, the European Central Bank was on course to withdraw its quantitative easing policies in the fourth quarter.

Timeline of Measures Opening the Capital Market

-Qualified Foreign Institutional Investors (QFII) Program launched in November 2002.

-Pilot scheme allowing foreign institutions to invest in the interbank bond market was launched in August 2010.

-The RMB Qualified Foreign Institutional Investors (RQFII) program was launched in November 2011 with an initial quota of 20 billion yuan.

-The RQFII quota was increased to 50 billion yuan in April 2012.

-The RQFII quota was expanded to 200 billion yuan in November 2012.

-More types of organizations were included in the RQFII pilot scheme in March 2013.

-The scope of foreign investors in the interbank bond market was enlarged in March 2013.

- Korea and Germany were included in the RQFII program in July 2014, with investment quotas of 80 billion yuan respectively.

-The Hong Kong Stock Connect program was officially implemented in November 2014.

-The pilot version of the Qualified Domestic Individual Investor (QDII2) program was put in place in six cities in June 2015.

-The process for overseas institutions of central banks to enter the interbank bond market was simplified in July 2015, and at the same time, the quota limit was cancelled.

-The Mainland-Hong Kong Mutual Recognition of Funds program was launched in November 2015.

-The QFII quota restriction was relaxed and the approval process simplified in February 2016. At the same time, the medium- and long-term institutional investors were allowed to enter the interbank market, with no quota limit.

-Insurance companies were allowed to invest in the Shanghai-Hong Kong Stock Connect in September 2016.

-The Shenzhen-Hong Kong Connect Program was launched in November 2016. In the same month, the first batch of investment management institutions was approved to manage pensions.

-Morgan Stanley Capital International (MSCI) index was introduced in the A-share market in June 2017. In the same month, the interim measures for the administration of Bond Connect were issued.

-Business Process for Overseas Commercial Institutional Investors to Enter China's Interbank Bond Market was issued in November 2017.

-The opening up of the financial sector was accelerated in April 2018, with relaxed restrictions on foreign capital and expanded business scopes for foreign financial institutions in China. In addition, the daily quota for the Chinese mainland and Hong Kong Stock Connect Programs was increased by a factor of four. In the same month plans were set for the Shanghai-London Connect Program and the QDII2 program before the year-end.

-SAFE and the PBOC issued notices in June 2018, abolishing the 20% ratio requirement for QFII fund remittance, scrapping the lock-up period for funds brought in under the QFII and RQFII programs and permitting QFII and RQFII investors to make use of foreign exchange rate hedging.

- Value-added tax on foreign institutions' interest income from onshore bond market investments will be exempted for three years, as clarified by an executive meeting of the State Council in August 2018.

The second factor was the rise in the price of Brent crude oil. Since the end of September, the price of Brent crude oil climbed rapidly from US$78 per barrel to US$86 per barrel, stimulating inflation expectations and pushing up long-term bond yields. (That trend has more recently reversed.) The third factor was a larger supply of US treasury bonds. US tax cuts convinced the US to issue larger quantities of treasury bonds, and the increased put upward pressure on bond yields. This highlighted the contradiction between a proactive fiscal policy and a tighter monetary policy.

US bond yields began to surge in late August, rising nearly 40 basis points. This rapid, short-term rise is likely to have a significant negative impact on inflows of international capital onto the Chinese bond market.

Stronger US Dollar

The US dollar's nominal effective exchange rate hit bottom and began climbing in late January. By mid-September it had advanced more than 10% year-onyear. Although it has fallen back slightly since then, it is still hard to see an end to the dollar's strength. As said before, the impact of the higher effective exchange rate of the US dollar on international capital inflows to the China's bond market will become more obvious after 3-6 months. The negative impact of this round of dollar strength should gradually be apparent.

Institutional Factors in China

While greater international capital inflows have their drawbacks, China is not likely to dwell on these negative aspects. The advantages of opening up China's capital market clearly outweigh the disadvantages. China will pay more attention to reforms such as enhancing the flexibility of the renminbi exchange rate and expanding the opening up of the bond market.

It is likely that between the second half of 2018 and the first half of 2019, there will be net inflows into China's bond market as a result of the continued opening of the domestic bond market and the internationalization of the renminbi. But the negative effect of higher yields on US long-term bonds and the rising effective exchange rate of the US dollar will limit those inflows.

The author is chief analyst for macroeconomics at China Merchants Securities Co. Ltd