Corporate fraud and bank loans:Evidence from china

2011-06-24YunsenChenSongZhuYutoWng

Yunsen Chen*,Song Zhu,Yuto Wng

aSchool of Accountancy,Central University of Finance and Economics,No.39,Haidian South District,China

bSchool of Economics and Business Administration,Beijing Normal University,China

Corporate fraud and bank loans:Evidence from china

Yunsen Chena,*,Song Zhub,Yutao Wanga

aSchool of Accountancy,Central University of Finance and Economics,No.39,Haidian South District,China

bSchool of Economics and Business Administration,Beijing Normal University,China

A R T I C L E I N F O

Article history:

Accepted 26 January 2011

Available online 27 August 2011

JEL Classification:

G32

G21

G38

Corporate fraud

Bank loans

Credit risk

Information risk

China

Receiving punishment from regulators for corporate fraud can affect financing contracts between a firm and its bank,as both the firm’s credit risk and information risk increase after punishment.By focusing on Chinese firms’borrowing behavior after events of corporate fraud,we find that firms’bank loans after punishment are not only significantly lower, but are also less than those for non-fraudulent firms.In addition,loan interest rates after punishment are not only higher than before,but also higher than those for their non-fraudulent counterparts.In addition,we find that corporate fraud indirectly destabilizes the‘‘performance-bank loan’’relationship.Our results suggest that corporate fraud negatively affects a firm’s ability to source debt financing,which provides new evidence about the economic consequences of fraud.

Ⓒ2011 China Journal of Accounting Research.Founded by Sun Yat-sen University and City University of Hong Kong.Production and hosting by Elsevier B.V.All rights reserved.

1.Introduction

This paper investigates the economic consequences of corporate fraud.This is of particular importance to investors and other market participants because of the rise in corporate fraud in recent years.For example,the acid waste incident involving Zijin Mining in July 2010 was disclosed 10 days after the event,which meant its investors lost the opportunity to sell their stocks in a timely fashion.Prior to this,the firm had already been investigated many times for poor information disclosure.1For example,Zijing Mining disclosed information on March 30,2010:‘‘For violation of the information disclosure regulation,we are being investigated by CSRC’’.According to the rectification report in December 29,2009,the Fujian Securities Regulatory Commission required Zijing Mining to improve its corporate governance mechanisms,including information disclosure,financial institutions and accounting processes,among others.Another example is Wuliangye Yibin,whose stock price fell by over 4%when it was held responsible by the Chinese Security Regulatory Committee(CSRC)for three fraudulent events:non-disclosure of important investment projects and losses, non-disclosure of important securities investment losses and data error on disclosed revenue.Some analysts,however,believe that the three events are old news and had no real effect on Wuliangye.2For more details,see the Finance and Economics website:CSRC disclose three faults of Wulianye.www.caijing.com.cn/2009-09-24/110259630.html.There are many instances of corporate fraud in the Chinese capital market,but many firms have not been affected and have no incentive to correct their behavior.Hence,thisresearch asks:does fraud have negative effects on firms?Most prior research related to the economic consequences of corporate fraud analyze the reason,mechanism and characteristics of corporate fraud(Beasley,1996;Chen et al.,2005a,b;Dechow et al., 1996;Johnson et al.,2009;Karpoff and Lott,1993;Karpoff et al.,2008;Zhang and Ma,2005)and the short-term market reaction (Chen et al.,2005a,b).Because of the limited refinancing ability of equity and debt markets in China,previous papers were unable to determine the long-term economic consequences of corporate fraud.As banks are the most important source of financing for listed companies in China,we can answer this question from the view of firms’borrowing behavior.

Disclosure of fraud and receiving punishment from regulators3Hereafter referred to as‘‘punishment for corporate fraud’’and‘‘violation of corporate regulations’’.influences the relationship between banks and firms by affecting credit risk and information risk.These events make banks anxious about a firm’s future cash flows and earnings,which affects their lending behavior to the firm.By focusing on firms who were punished for fraud in the Chinese A-share market during the period 2000-2007,this paper investigates the effects of punishment on the size and interest rates of bank loans.The results show that,compared with the situation before punishment,firms receive less bank loans and higher interest rates after punishment.In addition,compared with other firms,punished firms also receive less bank loans and higher interest rates. Moreover,corporate fraud also affects bank loans by influencing the relationship between bank loans and corporate performance indirectly.Our results show that punishment for fraud affects a firm’s ability to acquire financing.

This paper makes three contributions to the literature.First,it provides new evidence on the economic consequence of corporate fraud.Previous papers have focused on the causes,characteristics and short-term market reaction rather than the long-term economic consequences of corporate fraud.This paper,however,investigates the effect of corporate fraud on bank loans by investigating firms’credit and information risks,thus extending research on the economic consequences of corporate fraud.Second,due to the restrictions on equity financing in the Chinese capital market,bank loans are the main financing channel.This provides a good opportunity to examine banks’lending behavior after corporate fraud.Third, there is an upward trend in corporate fraud reported in recent years(Table 2).Hence,the results of this paper prove that Chinese regulators,such as the CSRC,are not a‘‘toothless tiger’’as punishment of firms affects their ability to source debt financing.

The rest of the paper proceeds as follows.Section 2 reviews the related literature.Section 3 presents our research hypotheses.Section 4 outlines our research design,and the empirical analysis is presented in Section 5.Section 6 concludes the paper.

2.Literature review

In the corporate fraud literature,researchers have focused on the characteristics and corporate governance mechanisms of the fraud firms,and also the short-term market reaction after a firm receives punishment.Beasley(1996)finds that more independent directors reduce the instances of corporate financial fraud,while the existence of an audit committee has no obvious effect.Dechow et al.(1996)find that firms whose chairman and CEO are the same person,having no controlling shareholders and having inside directors with shares are more likely to violate regulations.Johnson et al.(2009)use firms punished by the Securities and Exchange Commission(SEC)during the period 1991-2005 and investigate whether managerial incentives lead to fraudulent behavior.They find that managers in these firms have more restricted stocks,which means that managerial incentives are a major factor in committing fraud.Karpoff and Lott(1993)find that reputation loss is greater than the legal penalty in firms committing a crime,so in this situation the reputation mechanism is more important than the legal mechanism.Karpoff et al.(2008)examine firms who have financial restatement violations and find similar results as Karpoff and Lott(1993).However,Karpoff et al.(2005)find that firms who violate environmental regulations receive more legal and administrative penalties than reputation penalties.

In China,Chen et al.(2005a,b)use data during 2001-2002 to explore corporate governance and reputation mechanisms to discourage firms from committing fraud.They find that controlling shareholders can reduce the probability of fraud, while reputation mechanisms do not.Zhang and Ma(2005)find a positive relationship between corporate scandals and a firm’s controlling shareholder type and the chairman’s shareholding,but find no significant relationship between scandals and the number of board members,ratio of independent directors and institutional investors.Chen et al.(2006)find that ownership does not play an important role in corporate fraud.Wu and Gao(2002)examine how the market responds to punishment announcements from the CSRC during the period 1999-2000,and find that firms have a negative reaction after the punishment announcements.Chen et al.(2005a,b)find a similar result,and state that the CSRC is a‘‘tiger with teeth’’.

There is less research related to the economic consequences of corporate fraud,and the evidence is mixed.Using US data during the period 1981-1992,Agrawal et al.(1999)find that the disclosure of corporate fraud has no effect on executive turnover and corporate governance.Sun and Zhang(2006)find that in firms who commit corporate fraud,only the CEO gets punished while others get promoted after the turnover.Zhu and Wu(2009)find that fraudulent behavior increases audit fees,and the probability of non-standard opinions is more likely than before,but the level of fraud has no effect.

In summary,the literature on corporate fraud pays more attention to the determinants,characteristics and short-term market reaction,and there is little and mixed evidence on the long-term economic consequences of corporate fraud.Usingthe Chinese stock market,we attempt to contribute to the literature by investigating bank loans after a firm receives punishment for fraud.

3.Background and hypothesis development

The last 20 years has seen the rapid development of the Chinese capital market with regulatory policies giving listed companies improved access to financing.As protection of minority investors has also received increased attention,regulators have also been punishing fraudulent firms more severely and frequently.Regulations on corporate fraud have been improved with the enactment of laws such as the‘‘Security Law’’,‘‘Stock Issuing and Trading Act’’and‘‘Accounting Law’’,and IPO rules released by the Shanghai and Shenzhen Security Exchanges.Regulators in the Chinese stock market include the CSRC,the Shanghai Stock Exchange and the Shenzhen Stock Exchange.Both the enactment and enforcement of the law increase the cost of fraud for listed firms.However,some investors regard the regulators as a‘‘toothless tiger’’and their credibility is being questioned due to many instances of corporate fraud in recent years that have heavily damaged the interests of investors.Furthermore,in academia,the effect of punishment on firms who commit corporate fraud is still under debate.Chen et al.(2005a,b)find that firms who commit corporate fraud encounter a significant negative market reaction,but it is still unclear whether the punishment entails only an insignificant administrative penalty and short-term market penalty,or whether it influences other aspects of firms’activities,such as financing through bank loans.

As the Chinese stock market is not as efficient as that of developed countries,stock market reactions may not be a good indicator of the economic consequences of corporate fraud.In the Chinese capital market, firms face various restrictions on seasoned equity offerings and right offerings,and rely heavily on bank loans.Hence,examining the effect of corporate fraud on bank loans makes our test direct and important.For a bank,the most important consideration before contracting with a firm is to ensure that the firm has the capability to repay its loan.To guarantee enough cash flow in the future,banks are concerned about a firm’s operating and financial status.When the bank and the firm sign a lending contract,the bank will pay close attention to the firm’s credit/default risk and information risk and will consider the amount and quality of the firm’s future pro fits and cash flows.4Bharath et al.(2008)state that information risk is not the same as credit risk,as information risk originates from incompleteness and asymmetry of information,while credit risk is the probability of the firm violating an existing contract.Credit risk influences the mean of future cash flow,while information risk influences the variance of future cash flow.Credit risk mainly measures the quantity of future cash flows,while information risk mainly measures the variance of future cash flows.Once a firm is punished by regulators,the risk for the bank becomes higher, and the bank must increase its monitoring effort,which finally influences both the amount and the interest rates of loans.To summarize,fraudulent corporate behavior increases a bank’s credit risk and information risk and,thus,destabilizes the lending contract between the bank and the firm.

Specifically,an increase in credit risk can be generated by changing the bank’s belief,litigation responsibility and reputation loss,which further influence the lending contract.First,a fraud event directly affects a firm’s future real operating activities.As the most important creditor,the bank is concerned about a firm’s profitability and disclosure of a punishment for corporate fraud suggests that most of the information the firm released in the past is questionable,so the bank will probably change its judgment or belief towards the firm’s prior activities.To protect its interests,the bank may no longer offer the firm favorable terms of lending,and may also discount the available information about the firm’s performance.As a result,the bank may offer fewer loans and require higher interest rates.Second,most disclosure of corporate fraud is related to illegal actions.Unlike criticism from regulators,a firm who commits corporate fraud may also face litigation.This can lead to more sanctions from regulators,criticism from the public and restrictions from suppliers and customers,which result in the deterioration of both the operating and investing environment and further influences the firm’s future cash flows.All of these will affect lending from banks.Finally,Mailath and Samuelson(2006)prove the promotion effect of reputation in a long-term dynamic game.The lending contract is a game between a bank and a firm with stable expectations,and reputation saves on exchange costs.Corporate fraud behavior damages the good‘‘bank-firm’’relationship based on mutual reputation.As a result,the bank will approve fewer loans and require higher interest rates to avoid credit risk.

Besides credit risk,corporate fraud behavior can also influence a bank’s information risk.When contracting,the bank will considerinformation asymmetry.Bharath etal.(2008)find thataccounting quality can reduce information asymmetry in lending contracts.Yao and Xia(2009)find thatbanks can determine the quality ofa firm’sprofits.However,corporate fraud behavior increases the uncertainty ofa firm’s information and suggests other problems,such as problems ofcorporate governance,operating activities or controlling shareholder’s tunneling behavior.These make the bank more uncertain about the firm’s whole information environment and increase information asymmetry.As a result,the bank needs to monitor the firm more stringently,which increases monitoring costs and will be reflected as increased interest rates and a reduced quantity of bank loans.

In summary,punishment for corporate fraud will change a bank’s expectations of credit risk and information risk,and will further restrict the lending event by increasing interest rates and decreasing bank loans.These effects will not only be reflected as the difference in bank borrowing between before and after receiving punishment for corporate fraud,but also reflected in the comparison between fraud firms and their non-fraud counterparts.Hence,our hypotheses are as follows:

H1 After a firm receives punishment for fraudulent behavior,bank loans decrease

H1a For firms punished by regulators for fraudulent behavior,the increase in new loans will be less than in the prepunishment period

H1b Compared with non-fraudulent firms,the increase in loans will be less for fraudulent firms after receiving punishment

H2 After a firm receives punishment for fraudulent behavior,loan interest rates increase

H2a For firms punished by regulators for fraudulent behavior,the interest rates on its loans will be higher than in the pre-punishment period

H2b Compared with non-fraudulent firms,the interest rates on the loans of fraudulent firms will be higher after receiving punishment

When signing a contract with a firm,banks consider the financial status of the firm as one of the most important factors. Banks will use an effective monitoring system and its lending decision depends on the firm’s financial status.This results in a stable and suitable relationship between a bank and a firm.In fact,Hu and Zhou(2006) find an obvious positive relationship between bank loans and a firm’s financial status.Hu and Xie(2005) find that pro fit factors rather than liquidity factors in fluence short-term loans.Banks forecast future cash flows based on current performance to develop a stable‘‘bank loan-performance’’relationship.According to this,banks face both credit risk,which affects the quantity of future cash flows,and information risk,which affects the variance of future cash flows.Receiving punishment destabilizes the‘‘bank loan-performance’’relationship,and the bank doubts the firm’s performance and regards the punishment as a loss of reputation for the firm.This results in a discount on future cash flows,and thus will break the stable‘‘bank loan-performance’’relationship.In China where corruption is not as regular as in other countries,to avoid the risk,the bank has to pay more attention to the firm’s performance,which is often written explicitly in the lending contract.On one hand,disclosure of a punishment for corporate fraud directly affects lending behavior.On the other hand,the punishment destabilizes the‘‘bank loan-performance’’relationship and indirectly increases exchange costs.Basing on the above statements,we hypothesize that:

H3:Punishment for corporate fraud decreases firm’s positive‘‘bank loan-performance’’relationship and increases firm’s negative‘‘interest rate-performance’’relationship.

4.Research design

4.1.Models and variable definitions

From Table 1 we can see that the number of punishments for corporate fraud increases every year,which highlights the urgency and importance of this paper.The fraud types are classified as economic crime,illegal guarantee,illegal disclosure, false statement,delayed information disclosure,information missing or hidden and illegal tunneling.Among these,information missing or hidden,false statement and illegal disclosure constitute the majority of the sample(158,142 and 110 observations).Illegal guarantee has the least number of observations(21).

In the empirical sections,we investigate two types of comparisons of corporate fraud.First,we compare the time before and after the disclosure of punishment for corporate fraud,and then compare the bank loans received by firms punished for fraudulent behavior with those who do not commit fraud.We use loan renewals5To link bank loan changes to the corporate fraud behavior,we choose loans renewals excluding loans that firms already have(see Hu and Zhou,2006).and interest rates to proxy for the firm’s lending behavior,and the research models are as follows:

In model(1),we examine the direct influence of the disclosure of corporate fraud.In model(2),we use FR*ROA to investigate the indirect influence of fraud.CL is the change in bank loans in year t,considering the fact that in China there exists a‘‘Short-term loans for long-term lending’’phenomenon6For more details,see Wang et al.,2009.;besides CTL(all bank loans),we also use CSL(short-term bank loans). FFEE is the interest rate,measured as‘‘financing expense/(short-term loans+long-term loans+bonds payable)’’.7We also use financial fees from the cash flow statement as a robustness test.FR_1 is a dummy variable that takes a value of 1 if it is after punishment,and 0 otherwise;FR_2 is also a dummy variable that takes a value of 1 if the firm is punished in year t,and 0 otherwise.These dummy variables are used in the‘‘before and after the punishment’s disclosure’’subsample and‘‘whether or not punished in year t’’subsample,respectively.We control for the firm’s basic characteristics,such as performance,growth,cash flows,leverage,size,accounting information quality(earnings management and audit opinion),shareholdings of the first largest shareholder,ownership structure,and industry and year effects(Hu and Zhou,2006;Jiang and Li,2006).The definitions of the variables are presented in Table 2.

Table 1Time and type of the fraud sample.a

Table 2Variable definitions.

4.2.Data selection

Our sample comprises non-financial companies listed on the Shanghai and Shenzhen Stock Exchanges during the period 2003-2007.Data was collected from the CSMAR database.Missing data substantially reduces the number of observations we can use and the final corporate fraud sample is 729 firm-years.8If the firm is punished more than once in a year,we regard this as one observation in that year.There are 677 firms in the 729 firm-year observations;we include the situation that firms encounter several types of punishment in 1 year,so Table 2 has 768 observations.In the‘‘whether or not punished in year t’’subsample,using the matching method based on industry and size in the same year,we choose 729 observations for the non-punishment firm sample,9In a difference test of the two samples,the t value is 1.13,and Z value is 1.18.Both are not significant,which means our matched sample is successful.and examine their lending differences 1 year later.The former sample focuses on time-series comparison and the latter on cross-sectional comparison.10The cross-sectional comparison can reduce the errors influenced by firm’s lending strategy and not because of the fraudulent behavior.In a robustness test,we also use the full sample for comparison.All continuous variables are winsorized at upper and lower 1%levels to control for outliers.

5.Results

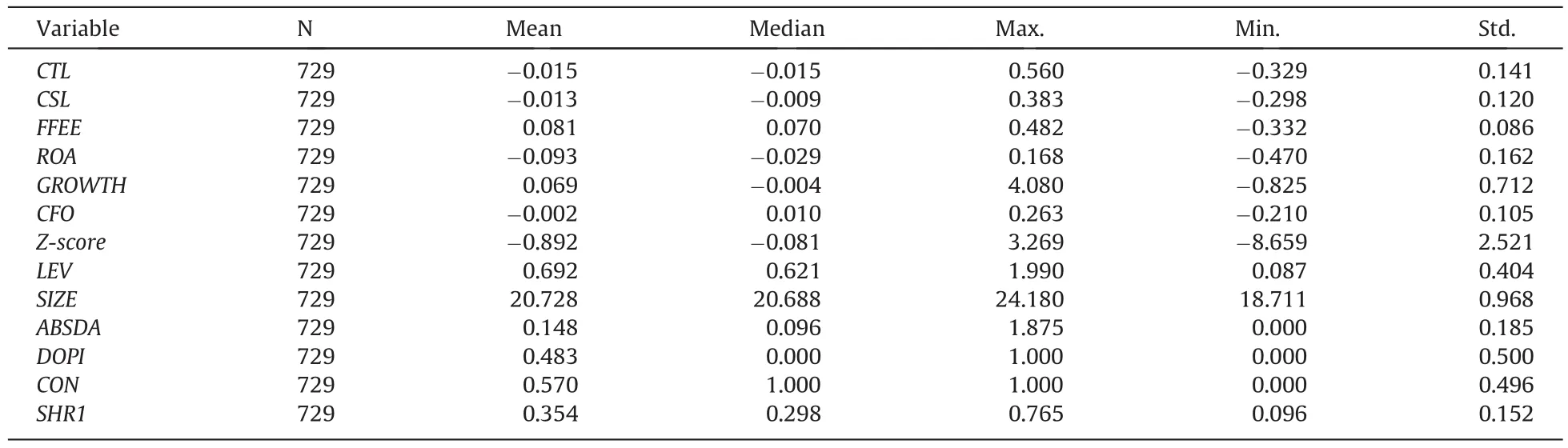

5.1.Descriptive statistics and univariate analysis

Table 3 shows the descriptive statistics.The mean of LEV is 69.2%,which means that the leverage of the fraud firms is much higher and bank loans are important for them.They should pay more attention to corporate fraud due to potentially high credit and information risks.The mean difference between CTL and CSL is small(-0.015 and-0.013,respectively), which means that there are a few long-term loans in Chinese listed firms.

In Fig.1,we set year t as the year that a firm receives punishment due to corporate fraud,and compare the differences in bank loans 2 years before and 2 years after.

Table 3Descriptive statistics.

Fig.1.Loan renewal changes before and after punishment for fraud.

From Fig.1 we can see that bank loans drop from year t-2 to year t+2.Intuitively,the consequence of corporate fraud is obvious.In fact,bank loans start decreasing in year t-1,probably because the fraudulent behavior has been committed before year t,although the regulators punish the firm in that year(regulators such as the CSRC have a time lag between paying attention to a fraudulent firm to informal investigation,formal investigation and releasing punishment),or a bank obtains information on fraudulent behavior before public investors do.We must emphasize that the change in bank loans is negative in years t+1 and t+2,that is,after the punishment the firm’s loans are lower than the year before and this trend is almost entirely due to the change in short-term loans.The results in Fig.1 indicate that corporate fraud behavior significantly influences bank loans,which preliminary supports our H1a.

Next,using univariate analysis,we compare total loan renewals,short-term loan renewals and interest rates of the two subsamples-‘‘before and after the punishment’s disclosure’’and‘‘whether or not punished in year t’’.Results are shown in Table 4.For the first subsample,compared with the year before punishment disclosure,the mean CTL and CSL is less in the year after the disclosure of the punishment,and the interest rate increases.The median results are the same(significant at the 1%level).The tests in Table 4 suggest that corporate fraud reduces a firm’s bank loans and increases its interest rate. Therefore,H1a and H2a are supported.Similar results are found for the subsample‘‘whether or not punished in year t’’, and H1b and H2b are supported.

5.2.Regression analysis

We first examine the subsample‘‘before and after the punishment’s disclosure’’,and the regression results are shown in Table 5.The relationship between FR_1 and CTL/CSL are significantly negative at the 1%level,and these results hold after controlling for economic and accounting quality factors.These results show that after the firm’s punishment disclosure, there is a decline in loans,which supports H1a.From the interest rate perspective,the relationships between FR_1 and FFEE are significantly positive at the 1%level,and these results also hold after controlling for economic and accounting quality factors.Hence,H2a is also supported.

We also find that ROA is positively related to CTL/STL and negatively related to FFEE,and all are significant at the 1%level. This suggests that the bank changes the loans based on the firm’s performance.However,the stable‘‘bank loan-performance’’relationship can be influenced by punishment for a firm’s fraudulent behavior,and this can be seen in Models 3, 6 and 9:the FR and ROA interaction term is significantly negative(Model 6),and the FR and FFEE interaction term is significantly positive(Model 9).In short,H3 is supported.

Second,we examine the subsample‘‘whether or not punished in year t’’,and the results are shown in Table 6.Consistent with Table 5,the coefficient on FR_2 is negative at the 1%level with CTL and CSL,but predominantly insignificant with FFEE.

Moreover,FR_2*ROA is negatively related to CTL/CSL and positively related to FFEE,which means that corporate fraud not only directly influences bank loans and interest rates,but also indirectly influences the‘‘bank loan-performance’’and‘‘interest rate-performance’’relationships.These results support H1b,H2b and H3.

Table 4Univariate analysis.

Table 5Results of‘‘Before and After the Punishment’’subsample.

Table 6Results of‘‘Whether or Not Punished’’sample.

5.3.Robustness tests

Considering that different firms have different borrowing strategies,we use dummy variables to measure bank loan renewals(Hu and Zhou,2006);that is,when CTL/CSL is positive,then DCTL/DCSL is 1,and 0 otherwise.The results of the logistic model are shown in Table 7.Similar to the OLS results,for both the subsample‘‘before and after the punishment’s disclosure’’and the subsample‘‘whether or not punished in year t’’,the coefficients on FR and FR*ROA are all negative at the 1%or 5%levels(except DCTL).Hence,all three hypotheses are further supported.

In addition,although a firm receives punishment in year t,its fraudulent behavior may be disclosed before that year,or the bank is more informed than the public.To control for this effect,we allocate the fraud year into the‘‘after fraud’’sample, and the results are shown in Table 8.FFEE and FR are significantly positively related,and CTL/CSL and FR are significantly negatively related.At the same time,to reduce errors when using the matching sample method,we add all non-fraud observations,and the results remain the same.

Meantime,we have also completed the following robustness tests(to be succinct,we do not present our results):

(1)In the subsample‘‘before and after the punishment’s disclosure’’,we only consider 1 year before and after the punishment’s disclosure.As in the‘‘bank-firm’’lending relationship,financial information is more important than other factors for the bank,so we also select the observations suffering financial fraud.Because banks may decide their lending behavior based on financial information,such as cash flow,growth,operating risk,financial information quality and leverage,we use comprehensive analysis to synthesize ROA,GROWTH,CFO,Z-score,Lev,SIZE,ABSDA and DOPI to a comprehensive variable.

(2)Considering that it takes a long time between the formal investigation by regulators and the disclosure of punishment, we delete observations where the interval between committing fraud and punishment is longer than 1 year.In addition,we add an interval variable to control for this effect in the OLS model.

(3)We also use‘‘cash outflow for financing expense’’in the cash flow statement to proxy for interest costs,as this variable is different from financing expense in the income statement and does not include items such as exchange gains and losses.

The results remain the same for these robustness tests,which means our results are robust.11We thank the anonymous referee for these suggestions.

Table 7Robustness test I.

6.Conclusions

Corporate fraud signi ficantly damages the interests of investors and punishment from regulators plays an important role in investor protection.However,does punishment for fraud have a negative effect on firms?This question is important not only to determine whether regulators are a‘‘toothless tiger’’or not,but also to protect investors and to promote the healthy development of capital markets.However,academic research has failed to form a consensus on this issue.

In contrast to the existing research,which mainly discuss the reasons and short-term market reaction to corporate fraud, this paper takes punished firms for corporate fraud as its research subject and focuses on changes in bank loans to investigate the economic consequence of corporate fraud.We believe that punishment for corporate fraud in fluences the contractual relationship between banks and firms,and affects the credit risk and information risk of bank loans.As a result,banks will be anxious about a firm’s future cash flows and earnings stability and,hence,will reduce the loans it will lend to the firm.Our empirical evidence shows that punishment for fraud reduces the amount of bank loans and increases the interest rate.Compared with non-fraudulent firms,fraudulent companies have lower bank loan renewals and higher interest rates. Moreover,corporate fraud in fluences bank loan policy by affecting the relationship between bank loans and performance.These results imply that punishment from regulators indeed has a negative economic impact on the subsequent bank loans of fraudulent firms.

The findings of this paper warn listed firms of the consequences of fraudulent behavior.We advise regulators to widen the range of punishments,and appeal to the media,investors and market participants to provide stronger supervision and apply more pressure on fraudulent firms.

Table 8Robustness test II.

Acknowledgements

The authors thank Donghui Wu(executive editor),the anonymous referees,Deren Xie from Tsinghua University,Xiongshen Yang,Donghua Chen,Xiang Li at the‘‘4th Doctorial Symposium of THU-SUFE-SZU-NJU’’,Minggui Yu,Qingyuan Li,Qiliang Liu at‘‘Luojia Young Scholar Seminar on Economics and Management’’in Wuhan University,Nutao Yu and participants at‘‘2010 Annual Academic Conference of Accounting Society of China’’for their helpful comments and suggestions.This study was supported by the National Natural Science Foundation of China(Project No.70772017),Scholarship Award for Excellent Doctoral Student granted by Ministry of Education,grants from the Beijing Municipal Commission of Education‘‘Joint Construction Project’’and the‘‘Project 211’’(Phase-3)Fund of the Central University of Finance and Economics,China.

Agrawal,Anup,Jaffe,Jeffrey F.,Karpoff,Jonathan M.,1999.Management turnover and governance changes following the revelation of fraud.Journal of Law and Economics 42,309-342.

Beasley,Mark S.,1996.An empirical analysis of the relation between the board of director composition and financial statement fraud.The Accounting Review 71,443-465.

Bharath,Sreedhar T.,Sunder,Jayanthi,Sunder,Shyam V.,2008.Accounting quality and debt contracting.The Accounting Review 83,1-28.

Chen,Gongmeng,Firth,Michael,Gao,Daniel N.,Rui,Oliver Meng,2005a.Is China’s securities regulatory agency a toothless tiger?Journal of Accounting and Public Policy 24,451-488.

Chen,Gongmeng,Firth,Michael,Gao,Daniel N.,Rui,Oliver Meng,2006.Ownership structure,corporate governance,and fraud:evidence from China. Journal of Corporate Finance 12,424-448.

Chen,Guojin,Lin,Hui,Wang,Lei,2005b.Corporate governance,reputation mechanism and the behavior of listed firms in committing in fraud.Nankai Business Review 6,35-40.

Dechow,Patricia M.,Sloan,Richard G.,Sweeney,Amy P.,1996.Causes and consequences of earnings manipulation:an analysis of firms subject to enforcement actions by the SEC.Contemporary Accounting Research 13(1),1-36.

Hu,Yimin,Xie,Silei.,2005.Bank’s monitoring effect and debt pricing.Management World 5,27-36.

Hu,Yiming,Zhou,Wei,2006.Creditors supervision:lending policy and corporate financial situation.Journal of Financial Research 4,49-60.

Jiang,Wei,Li,Bin,2006.Institutional environment,state-owned equity and bank lending discrimination.Journal of Financial Research 11,116-126.

Johnson,Shane A.,Ryan Jr.,Harley E.,Tian,Yisong S.,2009.Managerial incentives and corporate fraud:the sources of incentives matter.Review of Finance 13,115-145.

Karpoff,Jonathan M.,Lott Jr.,John R.,1993.The reputational penalty firms bear from committing criminal fraud.Journal of Law and Economics 36,757-802.

Karpoff,Jonathan M.,Lott Jr.,John R.,Wehrly,Eric W.,2005.The reputational penalties for environmental violations:empirical evidence.Journal of Law and Economics 68,653-675.

Karpoff,Jonathan M.,Lee,Scott D.,Martin,Gerald S.,2008.The cost to firms of cooking the books.Journal of Financial and Quantitative Analysis 43(3),581-612.

Kothari,S.P,Leone,Andrew J.,Wasley,Charles E.,2004.Performance matched discretionary accrual measures.Journal of Accounting and Economics 39, 163-197.

Mailath,George J.,Samuelson,Larry,2006.Repeated Games and Reputations:Long-run Relationships.Oxford University Press,Boston.

Sun,Peng,Yi Zhang,2006.Is There Penalty for Crime:Corporate Scandal and Management Turnover in China.EFA 2006 Zurich Meetings Paper,Peking University.

Wang Zhenwei,Zhao Dongqing,Zhu Wuxiang,2009.A empirical study on zero long-term loans of China’s listed companies.In:China International Conference in Finance.

Wu,Lina,Gao,Qiang,2002.A study of market reaction to the punishment bulletins.Economic Science 3,62-73.

Wu,Shinong,Lu,Xianyi,2001.A study of models for predicting financial distress in China’s listed companies.Economic Research Journal 6,46-55.

Yao,Lijie,Xia,Donglin,2009.Can banks in China see through firms’earnings quality?Auditing Research 3,91-96.

Zhang,Ji.,Ma,Guang,2005.Law,corporate governance and corporate fraud.Management World 10,113-123.

Zhu,Chunyan,Wu,Lina,2009.The auditors’reaction to companies’accounting and financial irregularities:analysis of the punishment bulletins of the CRSC, SSE,and SZSE.Auditing Research 4,42-51.

1 May 2010

*Corresponding author.Mobile:+86 13811048653.

E-mail address:chenyunsen@vip.sina.com(Y.Chen).

杂志排行

China Journal of Accounting Research的其它文章

- Macroeconomic control,political costs and earnings management: Evidence from Chinese listed real estate companies

- Why are social network transactions important?Evidence based on the concentration of key suppliers and customers in China

- Do modified audit opinions have economic consequences?Empirical evidence based on financial constraints☆

- Do institutional investors have superior stock selection ability in China?