On the Right Track

2020-02-17ByYuShujun

By Yu Shujun

As Chinas economic growth in 2019 slowed by 0.5 percentage point from the previous year and dropped to the lowest rate in nearly three decades, the debate about the future outlook for the worlds second largest economy has intensifi ed.

However, the 6.1-percent growth, as widely expected, was still in line with the governments annual target of 6-6.5 percent, according to the National Bureau of Statistics.

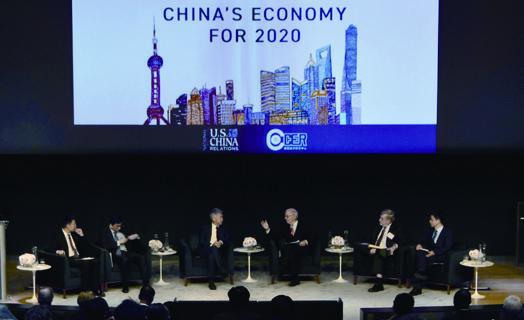

At the Forecast of Chinas Economy for 2020 conference hosted by the New Yorkbased National Committee on U.S.-China Relations and the China Center for Economic Research of Peking University (PKU) on January 9, economists from both China and the United States shared their observations on the Chinese economy. They believe that despite downward pressure, the economy still has the potential for steady growth.

Reasons behind slowdown

Both Chinese and U.S. panelists at the forum pointed out that the trade war is not a major factor behind the slowdown.

Nicholas Lardy, a senior fellow at the Peterson Institute for International Economics, said the trade friction has not had a very large effect on Chinas economic growth so far. Chinas exports in 2019 were roughly fl at, while global exports were down.“Were in an environment where global trade growth is very weak and China has done quite well. So it (China) has managed to offset a huge loss, roughly 20 percent, on exports to the United States, which is its largest market, by selling more to the rest of the world,” Lardy said.

He attributed the slowdown fi rstly to declining external surplus. Chinas global trade surplus has been shrinking in recent years after skyrocketing a decade earlier, which he thinks has been a drag on Chinas economic growth.

“Thats a major structural change, which I think, quite frankly, is a positive development,” he said.

Moderation of credit growth and misallocation of credit between state-owned companies and private companies are also factors causing the slowdown, according to him.

Xu Gao, Chief Economist at Bank of China International Co. Ltd., expressed similar views. “To a large extent, that decline[in Chinas economic growth] is not due to the trade war, but due to the harsh deleveraging policy implemented in the last two years,” Xu said.

“Because of the deleveraging, the credit growth and the total social financing in China slowed down signifi cantly and led to a credit crunch in the real economy. Private enterprises were particularly hit hard due to the credit crunch, which led to a decline in economic growth,” he added.

As the Chinese economy is entering a new phase of development, the financial problem appears to be growing, said Huang Yiping, an economics professor and Deputy Dean of PKUs National School of Development.

According to Huang, it has been said repeatedly, even in policy documents, that finance is not supporting the economy. A typical symptom is that private enterprises are fi nding it increasingly diffi cult to obtain funding.

Huang explained that Chinas economic growth, which used to rely on the low-cost advantage and low-end manufacturing, now needs to rely on more innovation and industrial upgrading, mostly done by private enterprises.

However, the fi nancial system, which is regulated by the government and dominated by the banking sector, is fi nding it very diffi cult to deal with new innovative private enterprises, most of which dont have good financial data, or adequate fixed assets or government guarantee.

“Theres a lot of money in the real economy, but its difficult to channel it from the fi nancial institutions to the corporate sector,” Huang said.

Government intervention in the Chinese financial system has often been blamed for this problem.

But Huang argued that government intervention is a transitional phenomenon, and its understandable.

Huangs research team found that government intervention under certain circumstances was helpful in supporting growth and fi nancial stability.

“If the regulatory framework is not welldeveloped, simply opening up [the fi nancial sector], liberalizing it and letting it go would actually create more problems than benefi ts,” he said.

In contrast to many emerging market economies which are prone to fi nancial crises, Chinas resource allocation, which may not be perfectly efficient, has maintained fi nancial stability, he said.

“But obviously, we need to go ahead,”he said, adding that further liberalization, reduced government intervention and market-based risk pricing are important measures.

In response to the financial difficulties of the private sector, the government adopted a series of policies in support of small and medium-sized enterprises and microbusinesses in 2019.

While a potential debt crisis is widely considered as the biggest risk to Chinas future growth, Xu said given Chinas high savings rate and not that high debt level in relative terms, it still has ample room to increase its debt-to-GDP ratio. “Chinese policymakers will use that room to maintain stable growth,” he said.

Xu forecast that Chinas GDP growth in 2020 is likely to remain stable at 6 percent, adding that the policy stance this year will be more geared toward maintaining stable growth, and a more friendly policy environment will boost economic growth.

Upside potential

Despite the slowdown and potential risks, panelists listed several factors that will shore up Chinas future growth.

Xu said the biggest upside potential for the Chinese economy lies in the massive number of high-skilled and low-cost workers.

Wang Xun and Wang Min, both from PKUs National School of Development, agreed that the ongoing urbanization process, which boosts consumption, investment and employment, will have a profound impact on Chinas future growth.

Barry Naughton, a professor at the University of California in San Diego and an economist focused on China, believes the economic impact of new technologies like artif icial intelligence, big data and 5G will be huge.

“The really big story is the integration of the broad Chinese market and these new technologies, which means people can be networked at a pace that weve never seen before,” Naughton said.

“China already has a 4G network throughout the countryside, which means that people who are still relatively poor are able to start businesses through Taobao and other online marketplaces, which is bringing a new boost of development to people who are based in relatively isolated places,” he said.

The Global System for Mobile Communication Association estimates that Chinese telecom operators would invest more than 1 trillion yuan ($145 billion) in 5G in the next fi ve years. According to Liu Duo, President of the China Academy of Information and Communications Technology, the value of information consumption driven by 5G commercialization in the country is expected to exceed 8 trillion yuan ($1.16 trillion) between 2020 and 2025, directly creating a total economic output of 10.6 trillion yuan ($1.5 trillion).

Financial opening up

For foreign investors, Chinas ongoing opening up of its fi nancial market has been bringing numerous opportunities.

“We are seeing concrete steps moving ahead,”said Huang, noting that the Chinese authorities announced 11 new measures to further open up the financial market in July 2019.

“The government is significantly reducing the limit for foreign financial institutions to get into the country,” he said.

Global financial services firms Nomura and J.P. Morgan Chase obtained their licenses in November and December 2019 respectively for doing securities business in China.

American Express joint venture won approval from the Peoples Bank of China (PBC) for setting up a bankcard clearing and settlement institution in November 2018, becoming the fi rst U.S. card network to gain direct access to the worlds biggest bankcard market. Its application for operation is waiting for the PBCs approval.

U.S. online payment company PayPal has offi cially entered the Chinese market after it fi nished acquisition of GoPay, a licensed payment company in China, in December.

On the market front, Chinese bonds were included into the Bloomberg Barclays Global Aggregate Index in April 2019. J.P. Morgan also decided to include liquid Chinese government bonds into its fl agship indices.

S&P Global Ratings has been permitted to establish and operate a credit ratings agency in Chinas domestic bond market.

Last year China removed investment quota restrictions for the Qualified Foreign Institutional Investor and Renminbi Qualified Foreign Institutional Investor programs. Foreign institutional investors with corresponding qualifi cations now only need to go through the registration procedure to remit funds independently to make securities investment.

“These are all happening. Whether or not theyre happening fast enough in order to maintain strong growth and gain effi ciency, Im confi dent and optimistic we are moving in the right direction,” Huang said.

(Reporting from New York City)