OPINION P2P Lending Requires Tighter Supervision

2015-11-28MaWeihua

OPINION P2P Lending Requires Tighter Supervision

Since Ppdai.com, China’s first peer-to-peer (P2P) lending company, was set up in 2007, the number of P2P lending platforms in the country has been growing rapidly.

By October 31, 2014, China had had a total of 1,474 P2P lending companies, and the lending amount had been far higher than that in the UK or the United States. This has certainly alleviated financing difficulties faced with small and medium-sized enterprises and promoted development of an inclusive financial system.

As an emerging innovative form of financial organizations, P2P lending also involves risks. For instance, many of such platforms have suddenly gone missing, causing losses to investors and casting a slur on the reputation of the industry.

One of the main reasons for the chaos in the P2P lending industry is a lack of supervision. Since April 2014 when the China Banking Regulatory Commission (CBRC) was designated as the leading supervisor of P2P lending, it has put forward 10 supervision principles, including the intermediary nature of P2P lending platforms and prohibitions on offering guarantees or creating their own capital pools.

However, there are no detailed supervision rules and the industry mainly relies on self-discipline. To protect investors’ interests, guide sound development of the industry and promote financial reform and innovation, the government should urgently draw up detailed supervision rules. Recently, the CBRC has decided to reform its organizational structure, establishing a department of inclusive finance for the administration of P2P lending businesses.

I think it is necessary to formulate supervision rules as soon as possible to encourage and guide the establishment of industrial selfmanagement organizations and third-party evaluation and consultation institutions. The supervision rules must include the access and exit rules for P2P lending platforms, the supervision on operations of P2P lending platforms and requirements on information disclosure by P2P lending platforms.

I suggest the government formulate and implement access and exit rules for P2P lending platforms. These platforms are important to the market, and they should also be subject to government supervision. Strict control of qualifications of P2P lending platforms will be conducive to controlling the risks of the whole industry. Detailed qualifications can include the following requirements: Shareholders and management teams of such platforms must not have any record of bad behavior and have enough financial knowledge and experience; P2P lending platforms must have offices, IT facilities and risk control systems to ensure network technology safety; and the supervising authority may establish different terms of access for platforms with different operation models.

The government should supervise the operations of P2P lending platforms. Classified supervision may be used, and the lending products on the platforms must be subject to supervision. Funds of the clients and capitals owned by the platforms must be separated. Clients’ funds must exist within the custody of third-party institutions. The flow of funds is subject to government supervision, so as to prevent diversion of clients’ funds, illegal fundraising, fraud and money-laundering. Third-party institutions should also be qualified and ready to act upon approval.

The government should also supervise information disclosure by P2P lending platforms. It can require disclosure of the following information: corporate governance, operation models, risk control systems, regular business data as well as basic information on credit and lenders. The platforms are also obliged to ensure safety of the information.

Finally, the government must encourage and guide the establishment of industrial self-disciplinary organizations and third-party institutions. While improving supervision, the P2P lending industry should also set up self-disciplinary organizations. At present, such organizations in China are not well developed. Industrial standards on information transparency and sharing are needed. Moreover, the supervising authority must strengthen investor education, cultivate a rational investment philosophy among them and improve their awareness of risk prevention. The government should also encourage the development of quality third-party evaluation and consulting institutions to reduce risks in the industry.

This is an edited excerpt of an article by Ma Weihua, a member of the 12th National Committee of the Chinese People’s Political Consultative Conference, published in Economic Information Daily

NUMBERS

($1=6.12 yuan)

66%

Growth of net revenues of JD.com, a major Chinese e-commerce company, in 2014

$8.44 bln

The amount of money China’s financial institutions received in net foreign direct investment in 2014

2.1 bln yuan

The amount of money China’s Central Government provided in 2014 to support press and publishing projects

274 mln

The number of farmerturned-laborers in China as of the end of 2014; 168 million of them had moved to cities as migrant workers

39,881

The number of China’s valid licenses to fly civil aircraft as of the end of 2014

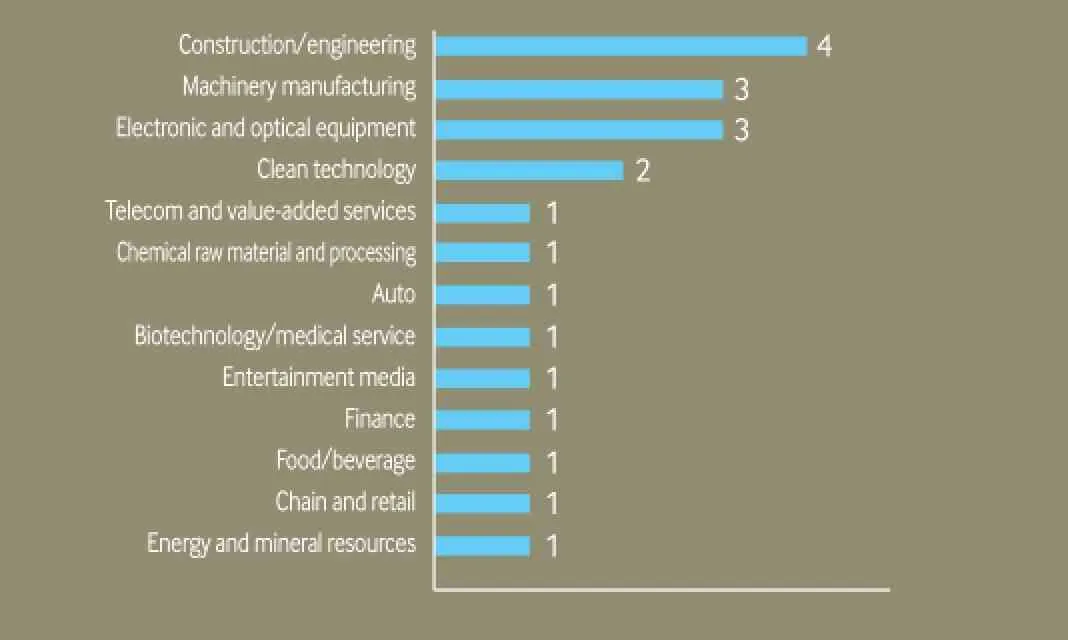

Number of Chinese Companies' IPOs on Mainland Stock Exchanges by Sector, Feb 2015

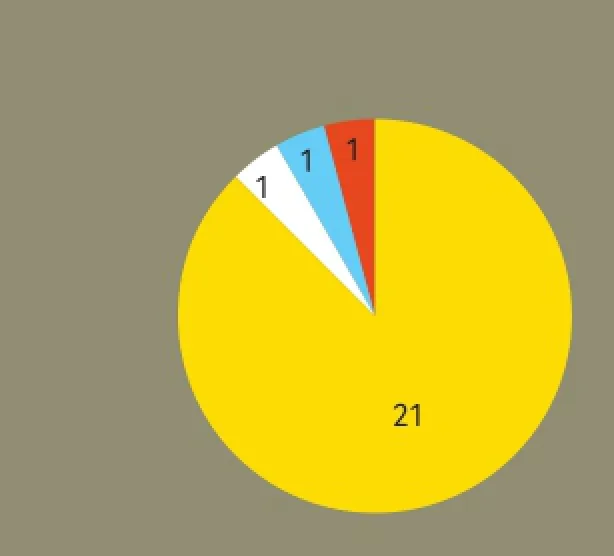

Chinese Companies' IPO Distribution, Feb 2015

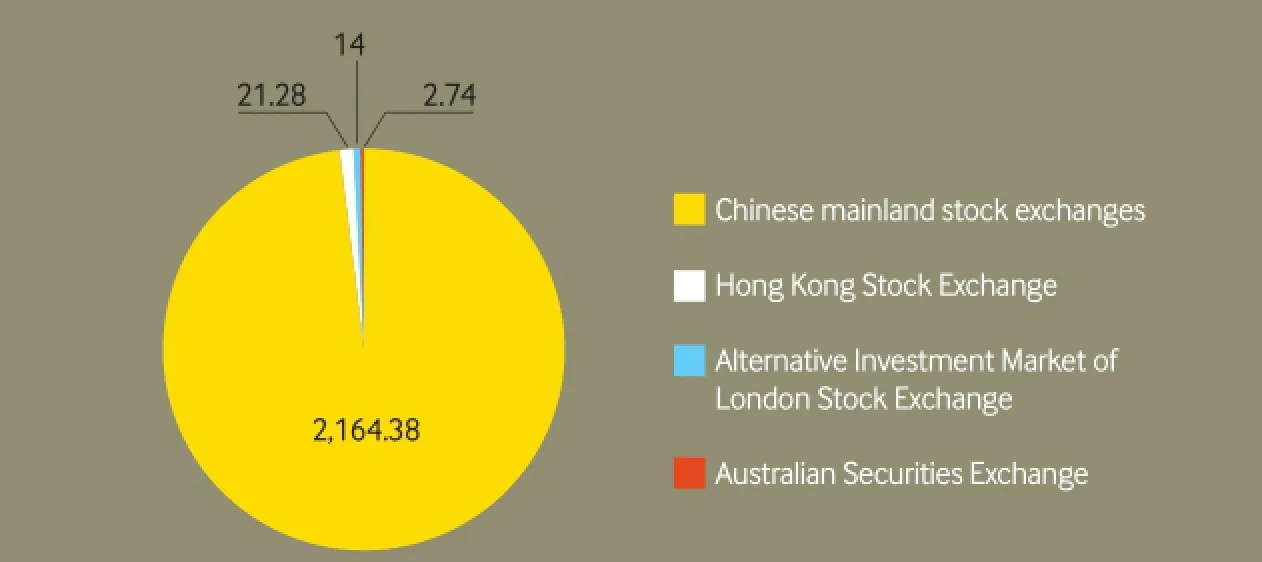

Financing Amount of Chinese Companies' IPOs, Feb 2015 ($mln)

1.3%

year-on-year growth rate of auto sales of General Motors Co. and its joint ventures in China in February

14.6%

year-on-year drop of retail sales in Hong Kong in January

19%

The average increase in minimum wage in south China’s Guangdong Province, which will start on May 1