Remaining Vigilant

2014-07-28ByAnnLee

By+Ann+Lee

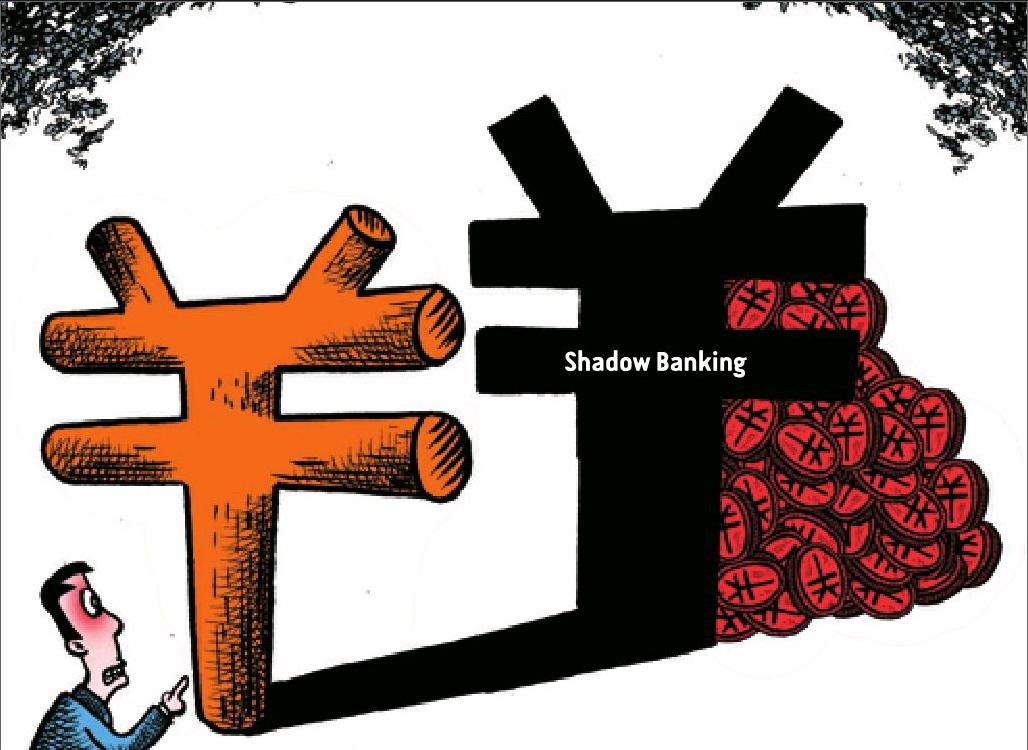

The topic of shadow banking has now become the topic du jour of what will crash the Chinese economy. Before that, it was the real estate bubble, and before that, the rising cost of cheap labor. Of course, many wrong predictions later, the bears of China continue to prognosticate that China will crash because they have a vested interest in seeing China crash. I am not going to say that China will never hit a speed bump. In fact, I think that scenario is likely, but not for the reasons that the China bears often use. But first, the shadow banking issue.

I will not reiterate all the problems that are going on with Chinas financial system. I have heard them all, ranging from falsified trade receipts to excessive loans by the local government to record high corporate bond underwriting that would presage an inability to repay bank loans. All I can say is that as soon as one of these problems is addressed, new ones will pop up so this will be a never-ending cycle of financial issues as long as the financial system becomes more and more open and permissive like its Western counterparts. Human creativity is infinite, and therefore there is no limit to the number of financial products that people can invent to bypass existing rules and regulations. Thus the problem is not the different schemes that the shadow banking community can develop that can get out of hand, but the ability of the authorities to address the problems once they are discovered.

The reason I am more sanguine about Chinas prospects than the average China bear is two-fold. First, the Chinese Government, like that of the Federal Reserve, has the power to print money. This is a very powerful tool at their disposal because it enables the economy to avoid a full-blown depression. Many other countries do not have this ability because their governments do not have the credibility with the rest of the world to simply print more of their currency. If they do, they just create hyperinflation within their borders, which doesnt solve anything because other countries will not accept its inflated currency. But in the case of the United States, and also of China, the rest of the world will continue using dollars or the renminbi, at least for the foreseeable future, because these two nations are too interconnected with the global economy and thus can continue with business as usual even if their central banks decide to use the printing press to fix a temporary problem.

If we look at what is happening in the U.S. financial system, post-2008 financial crisis, we see that the exact same behavior is happening on Wall Street as the years leading up to the crisis except that the bad behavior is even more magnified than before. The banks continue to underwrite record amounts of structured products, and the underwriting is even shoddier. Whereas the problem before the crisis was that a lot of collateralized bond obligations were “covenant lite,” meaning that there were very few restrictions on the borrowers, today these financial products largely dont even have covenants. This has led to enormous bonuses on Wall Street again by both the investment bankers and the private equity firms who have borrowed the money to acquire expensive companies and resell them to the public stock market at even higher valuations. Anyone familiar with the reasons for the 2008 financial crisis understands that the same exact bubble is being replicated, yet no one is worried this time because everyone knows that the Federal Reserve will bail everyone out if something blows up again.endprint

Even the prospect of another bubble bursting in the United States from the unsustainable underwriting that has been allowed to continue hasnt stopped the rest of the world from doing business with the United States. Everyone knows that the Federal Reserve has printed trillions of dollars since the 2008 financial crisis to keep some key financial institutions from going out of business and will continue to do so for a very long time. Money growth has far outstripped economic growth, and while this monetary policy seems irresponsible to certain critics who fear the growing prospects of either hyperinflation or permanent wealth inequality and class immobility, the bottom line is that the United States can get away with it without being knocked off its perch as a superpower.

Likewise, Chinas monetary authorities have the same tools and power at their disposal. Since Chinas financial system still has capital restrictions that limit hot money flows and is not dependent on borrowing money from other countries to keep its economy growing, it is not as vulnerable to debt problems in the same way that the United States is largely immune from them. Since Chinas debt problem is mostly domestic, the Chinese monetary authorities can simply print money to take care of bad loans just like the United States has done. This power is unlike those in many other countries such as those in the eurozone who have to borrow money in a currency that they have no sovereign control over. Some high profile defaults in China may temporarily worry some investors, but they will come to pass in the same way that investors in the United States like Warren Buffett stopped worrying about the U.S. markets after Lehman collapsed. In the case of China, any financial problem will unlikely be as magnified as the crisis of 2008 since renminbi products are nowhere as ubiquitous as dollar-denominated financial products and the Chinese authorities have learned from what the U.S. Fed, the European Central Bank, the Bank of England, and the Bank of Japan have done to address financial stability issues these last few years.

However, if China does lose its ability to generate internal growth from its real economy and if China is no longer competitive on the world stage, then yes, my earlier reasoning will unlikely hold true. Since China does not have the worlds strongest military nor the strong global network of allies that the United States has built, it cannot influence the rest of the world to use its currency the same way that the United States can. Since China does not have this power, it must be vigilant to ensure that its financial economy doesnt overtake its real economy. If Chinas financial economy ever becomes too dominant, then the country will be generating lots of profits on a short-term basis, but no real wealth for the long run. In essence, paper profits from financial services are just a house of cards because they dont create lasting infrastructure or real knowledge for improving the well-being of people or the environment. If China goes down that path, such a scenario could eventually erode confidence from other countries and thus spell the end of Chinas rise. While I do not think the current Chinese Government will be this na?ve and short-sighted, I concede that it doesnt take that many bad eggs who have the political power to persuade policymakers to do the wrong thing.endprint

Some may also wonder why China must do the heavy lifting of hard work in the real economy when the Europeans and the Japanese also print exorbitant amounts of money with debt ratios that are much higher than Chinas and also do not have strong militaries. The reason is that the United States views both the Europeans and the Japanese as allies while it currently sees China more as a threat. Since these American allies are not viewed as potentially challenging American superiority, they have more freedom and time to act as they desire to suit their interests without inviting American suspicion. Because of this political reality, the Chinese cannot assume that they are playing on an even global financial playing field.

So like any flawed argument, China cannot collapse if only one side of the equation is weak. As long as viable solutions are available to address problems, then nothing too serious will happen. Only when both sides of the equation, the regulators and the regulated, are broken and out of options will the whole system come tumbling down.endprint