THE RENMINBI AS GAME CHANGER

2014-02-25ByAnnLee

By+Ann+Lee

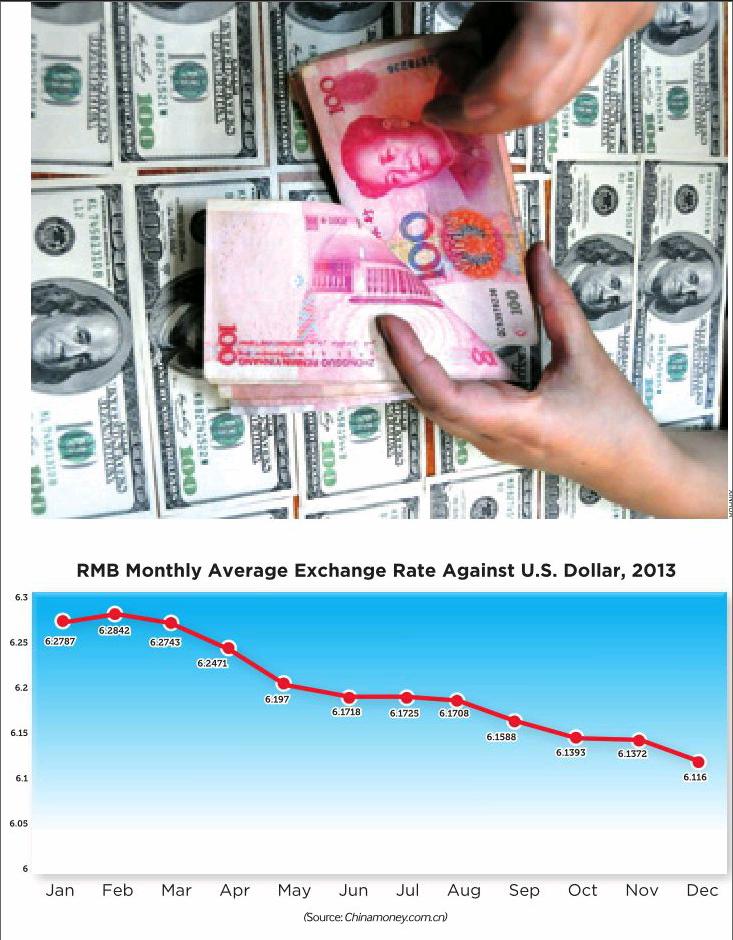

The announcement of the Shanghai Free Trade Zone, which heralds Chinas plans to liberalize the financial economy, has been seen as a welcome indication by most Western financial firms who have been pressuring China for years to allow unrestricted convertibility of its currency, the renminbi. This announcement follows a historical pattern of U.S. policy pressure on other countries monetary management such as when the United States pressured Japan to float its currency in 1973 after the U.S. unilaterally abandoned the gold standard in 1971.

A free floating currency, especially from an economy as large as Chinas, is conventionally seen by financial mavens as the last great frontier for rapid profits from foreign exchange trading. Wall Street is salivating and cannot wait for this market to reach takeoff. But while the financial benefits that will accrue to Western financial firms in the short term will be unmistakable, Chinas move to internationalize the renminbi could actually rival the U.S. dollar in our lifetime.

Since the end of World War II, the U.S. dollar has enjoyed the primacy of being a world reserve currency and continues to do so. About two thirds of all international transactions are conducted in U.S. dollars and a large number of nations rely on financing from U.S. credit. Thus, many countries shudder at the thought of the U.S. Federal Reserves tightening since the easy credit that flows to their shores can suddenly dry up and cause a credit crunch that in the past has resulted in the Asian crisis, the Russian crisis, and more recently the 2008 global financial crisis.

However, reliance on the U.S. dollar is slowly being eroded as countries seek to avoid being vulnerable to such credit shocks. The growing use of the renminbi in many parts of the world for trade settlement and even loan growth will slowly marginalize the U.S. dollar. Thus, when the Fed finally implements the tapering off of its extraordinarily loose monetary policies, instead of creating another Asian crisis as it did in 1997 or other similar panics, these nations will likely find alternative sources of credit in the form of Chinas renminbi to keep their economies running smoothly.

While the other alternative reserve currency, the euro, can also function as an alternative source of credit, the European Union will face considerably more challenges in getting consensus on European-wide bank regulation given the highly variable political challenges across the member states. China, on the other hand, can act more quickly and decisively as one nation in the credit markets should another international financial crisis befall the world, and this ability could quickly challenge the supremacy of the U.S. dollar in international transactions.endprint

Many argue that the U.S. dollars status as the world reserve currency is guaranteed for the foreseeable future given the strong fundamentals of the U.S. economy and its military that is second to none. Though no one denies U.S. military superiority, the fundamentals of the U.S. economy are far more questionable if one examines its long term prospects.

First, the political will needed to reign in deficit spending is nonexistent. With annual tax revenues of $2.2 trillion, but transfer payments for such entitlement outlays as pension and unemployment amounting to $2.4 trillion every year, the United States is already $200 billion in the hole without spending a single dime on any of the other government services. Once the other government spending such as military is added to the annual budget, the United States will face deficit spending north of $1.3 trillion every year.

With U.S. total debt exceeding $60 trillion, no one actually believes that the United States will ever pay its debt obligations. The avoidance of much needed infrastructure spending such as a high-speed train between Boston and Washington D.C. that can improve American productivity compounds American slippage in competitiveness.

Finally, the much discussed problems in Americas K-12 public education as well as the uselessness of many college degrees from many U.S. colleges and universities undermines the ability of American labor to keep up with competition from global talent. The long held view that U.S. innovation will be Americas trump card may also turn out to be a case of the emperor with no clothes. Americas social media websites does little to improve the welfare of citizens; Apple products are losing their allure without Steve Jobs; and Teslas electric cars may prove to be nothing but toys for the wealthy. Even fracking shale gas will have its limits. The only way to ensure that natural gas will continue to be produced in the United States is if there is enough demand to absorb the huge supply. Creating enough demand will require the United States to export natural gas by liquefying it into LNG and making it usable at the destination. However, the process of creating LNG adds so much additional cost to U.S. natural gas that other nations will no longer see it as a compelling source of energy.

Without strong economic fundamentals, more and more polite company will agree that the U.S. dollar is highly overvalued and at risk of going into freefall.endprint

Of course, the U.S. buildup of its military is intended in part to coerce nations from aban- doning the use of the U.S. dollar. The threat of military action on the part of the United States to maintain the status quo is no different than the coercive tactics used by imperial colonialists of earlier centuries to extract goods and services from developing countries without reciprocal exports. Everyone knows that the United States imports far more than it exports, and this trend shows no sign of reversing course as U.S. manufacturing continues to decline rapidly toward the single-digit percentage of GDP. The problem of relying on its military threat, however, may be effective against smaller nations, but would be suicidal against China. With Chinas trading partners and allies spanning the entire globe, U.S. military retaliation against China could easily invite the wrath of the entire world. No matter how superior the U.S. military is, it cannot wage war against billions of people and be certain of success.

Certainly no one wishes the U.S. dollar to depreciate suddenly and massively. Such a calamity will stop cross-border trade instantaneously and would inflict more harm than Lehmans collapse. Even the Chinese, who hold over $1 trillion in foreign reserves largely in U.S. Treasuries, hope never to see that day. But the fact that the Chinese recognize that such a scenario is not impossible, they certainly now see the need to accelerate the internationalization of the renminbi as serving their own interests as much as it serves the interests of Wall Street.

By providing the world with an alternative credible currency with the economic fundamentals to support its use, Chinese credit could displace the use of U.S. credit in a material way for the first time since Pax Americana. If that happens, the days that the United States can maintain consumption levels at 70 percent without inflation will be numbered.endprint