Banking system reform,earnings quality and credit allocation

2012-06-27XiuliZhuLinjunLiYunkuiXue

Xiuli Zhu,Linjun Li,Yunkui Xue

aNanjing University of Finance and Economics,China

bShanghai Jiaotong University,China

cCheung Kong Graduate School of Business,China

Banking system reform,earnings quality and credit allocation

Xiuli Zhua,b,*,Lianjun Lia,Yunkui Xuec

aNanjing University of Finance and Economics,China

bShanghai Jiaotong University,China

cCheung Kong Graduate School of Business,China

A R T I C L EI N F O

Article history:

Accepted 28 August 2012

Available online 9 October 2012

JEL classification:

G3

G32

G38

Banking system reform

Ownership

Earnings quality

Credit allocation

This paper investigates credit allocation before and after the 2003 banking system reform in China.We find that relationships between earnings quality and new short-term loans,long-term loans and total loans in listed companies changed significantly after the banking system reform,especially in stateowned listed companies.Further investigation shows that due to the influence of rent-seeking,banks have eased the earnings requirements of non-stateowned listed companies.These findings enhance our understanding of the economic consequences of the banking system reform and of credit discrimination under the new regime.

Ⓒ2012 China Journal of Accounting Research.Founded by Sun Yat-sen University and City University of Hong Kong.Production and hosting by Elsevier B.V.All rights reserved.

1.Introduction

Government intervention in the financial system to promote the development of the capital markets is one of the distinguishing characteristics of China’s transitional economy.Theorists and practitioners have long held that ownership is an important factor that determines China’s financial resource allocation and that thereis serious non-equilibrium credit rationing1In contrast to non-equilibrium credit rationing,equilibrium credit rationing is due to information asymmetry or customer relationships (Jaffee and Russell,1976;Williamson,1986).in China’s credit market with discrimination against non-stateowned enterprises(Brandt and Li,2003;Cull and Xu,2005;Sun et al.,2005).Relative to state-owned enterprises,the financial resources obtained by non-state-owned enterprises do not support the value created or“ownership determinism”theory.However,Fang(2010)implies that the financial discrimination that nonstate-owned enterprises suffer is more likely to be due to their own strategy decisions or“corporate decisions”theory.

However,due to the mandatory change in China’s financial market,commercial banks and borrowers have long been active participants in the market and thus research on credit resource allocation should pay more attention to the rent-seeking of banks that originates from their monopoly.Xue and Zhu(2010) find that the financial reform at the end of 2003 did not affect property rights arrangements,nor did it change banks’forecasts of soft budget constraints,as borrowers’debt maturity choices depend on banks’rent-seeking characteristics.This paper takes ownership into account and studies whether state-owned enterprises and non-stateowned enterprises had different credit sources during the process of institutional change,whether banks’ rent-seeking affects the loan allocation structure and whether the banking system reform has promoted the marketization of credit resource allocation.

We investigate credit allocation efficiency before and after the 2003 banking system reform and find that since the banking system reform,the role of earnings quality has been enhanced in the credit market and the relationships between earnings quality and new short-term loans,long-term loans and total loans have changed significantly in listed companies,especially in state-owned listed companies.Further research implies that due to the influence of rent-seeking(Xue and Zhu,2010),commercial banks have loosened the earnings requirements of non-state-owned listed companies.

The remainder of this paper is organized as follows.Section 2 discusses the related literature and hypotheses.Section 3 covers the data,variables and descriptive analysis.Section 4 provides the empirical methodology and presents the empirical findings and robustness tests,and Section 5 concludes.

2.Related literature and hypotheses

2.1.Impact of soft budget constraints and banks’rent-seeking on credit allocation

When legal systems are weak,government regulation and financial intervention may be external constraints to running financial markets in emerging economies.Due to socialist governments’“father complex”toward state-owned enterprises(Kornai,1980;Kornai et al.,2003)and government compensation for policy loss during transition periods(Lin et al.,1994/1999,1997,2004),governments tend to relax financial discipline and soften budget constraints(Kornai,1980).When state-owned commercial banks themselves benefit from soft budget constraints and expect the government to redeem them,they will inevitably weaken its oversight role. Further,the increased government-backed interest may result in bankruptcy,harm owners’benefits and generate enormous social costs(Akerlof and Romer,1993).This in turn leads to more widespread soft budget constraints(Berglof and Roland,1995).Gao and Schaffer(1998)find that in transition countries,soft budget constraints give unprofitable enterprises access to bank credit more easily,thus the resource allocation efficiency of the banking system is lower.Studies on China’s financial market show that ownership and political relations are important in giving enterprises access to long-term loans,with state-owned enterprises receiving more long-term loans at lower credit standards(Sun et al.,2005;Jiang and Li,2006;Zhang et al.,2010).

Before the banking system reform,a dual soft budget constraints mechanism2Soft budget constraints contain at least two subjects:the constrained object and the supporter(Kornai et al.,2003).Constrained objects are limited by their own resources.If they make a loss,then they will not survive without external aid.Supporters are controlled by government and can transfer resources to aid troubled firms.After January 1,1985,China’s commercial banks replaced fiscal appropriation and became supporters of soft budget constraints,whereas the Central Bank became the supporter of the commercial banks and an eventual lender to state-owned enterprises and banks,creating a dual soft budget constraint.substituted for a creditor protection mechanism,which to a certain extent reduced the commercial banks’losses but caused state-ownedcommercial banks to neglect their credit risk control,which led to more serious soft budget constraints.The mixed property rights between state-owned commercial banks and state-owned listed enterprises induced some state-owned enterprises to regard credit loans from state-owned commercial banks as“free capital.”Once they obtained such loans,diversion and embezzlement were inevitable.3There were widespread problems in the restructuring of state-owned enterprises and borrowers diverted and embezzled their debt in the weak legal environment,harming creditors’interests.At the same time,state-owned commercial banks that had a monopoly over financial resources inevitably sought rent,which resulted in a large number of“relation-loans”or“corruption-loans”and eventually produced a large amount of non-performing loans that had to be borne by the government.Negotiation between banks and enterprises led not only to“state-owned enterprise escape,”but also to“non-state-owned enterprise escape.”In the long run,state-owned commercial banks’exclusive monopoly over financial resources caused serious corruption,which threatened China’s financial stability(Xie and Lu,2005).

2.2.Impact of the banking system reform on budget constraints

Before 2003,China’s financial market reform mainly served the development of the capital market and did not display characteristics of independence and marketization.The dual soft budget constraint and rent-seeking behavior led state-owned commercial banks to the edge of“technical bankruptcy”(Xie and Lu,2005).The Chinese government responded with a new round of financial reforms at the end of 2003 that involved the following aspects.(1)Capital injection and financial restructuring-at the end of 2003 and beginning of 2004,the Bank of China and the China Construction Bank received injections of US$22.5 billion and US$45 billion,respectively,of foreign exchange reserves and sold US$278.7 billion of suspicious bad assets to Xinda Assets Management Companies.On November 6,2008,Central Huijin Investment injected US$19 billion into the Agriculture Bank of China.In April 2005,Central Huijin Investment injected US$15 billion into the China Industrial and Commercial Bank.By 2005,the proportion of non-performing loans of these banks had fallen to below 5%and their capital adequacy ratio had reached the 8%required by the Basel New Capital Accord(Basel II)of 2006.(2)Corporate governance system improvement-according to“Guidance on the Corporate Management of Joint-stock Commercial Banks”released by the People’s Bank of China in June 2002,“Guidance on the Corporation Governance Reform and Supervision of Bank of China and China Construction Bank”released by the China Banking Regulatory Commission in 2004 and“Guidance on the Corporation Governance Reform and Supervision of Stated-owned Commercial Banks”released in April 2006,the three banks set up a corporate governance structure and introduced international investment banks as strategic investors to optimize the shareholding structure.(3)Exchange listings-after a series of capital injections,financial restructuring and the issuance of new shares,China Construction Bank listed on the Hong Kong Stock Exchange on October 27,2005;the Bank of China listed on the Hong Kong Stock Exchange on June 1,2006 and on the Shanghai Stock Exchange on July 5 of that year,and the China Industrial and Commercial Bank listed on both the Shanghai and Hong Kong Stock Exchanges on October 27,2006.The Agricultural Bank of China Co.,Ltd.was established on January 16,2009 and listed on the Shanghai and Hong Kong Stock Exchanges on July 15 and 16 of that year,respectively.(4)Financial legal system construction-to ensure the smooth reform of the financial system,the sixth meeting of the NPC Standing Committee promulgated the“Law of the People’s Republic of China on the People’s Bank of China (Revised)”,the“Law of the People’s Republic of China on Commercial Banks(Revised)”and the“Banking Supervision Law of the People’s Republic of China.”The three laws were executed in early 2004.The People’s Bank of China and the China Banking Regulatory Commission either individually or jointly issued nearly 60 regulations and guidelines in 2004.

Wu and Bai(2009)find that the financial system reform at the end of 2003 significantly tightened budget constraints,but due to the mandatory nature of the reform the economic system retained automaticity during the reform period(Aoki and Okuno,2005).Xue and Zhu(2010)note that the financial reform,bound by the cost-benefit balance of state-owned banks and enterprises,has not alleviated banking corruption.

According to the foregoing analysis,before the reform there was a weak legal environment,soft budget constraints and banking corruption in China’s financial market.After the reform,the soft budget constraints were eased,but the rent-seeking behavior of banks was not totally resolved.Thus,it is particularly important to study the relationships between banking reform,banking corruption and credit discrimination.This paper focuses on two aspects of these issues:the change in the relationship between ownership and access to loans after the financial reform and the difference in total loans between state-owned enterprises and non-stateowned enterprises after the financial reform.

2.3.Impact of financial reform on the decisions of lenders and borrowers:Hypothesis 1

It has been proved that earnings quality has a significantly negative influence on the cost of capital(Francis et al.,2002,2003,2005;Chow,2008).According to the foregoing analysis,the mandatory reform was triggered not only by government,but also by the urgent need for the development of the financial market at this stage.In the long run,market-oriented resource allocation is not only needed by listed companies and commercial banks,but is also a fundamental way to improve the efficiency of resource allocation.After the reform, along with the improvement of the legal environment,the quality of accounting information became more important to credit resource allocation.This is summarized as hypothesis 1.

H1.The banking reform enhanced the role of earnings quality in market-oriented credit resource allocation.

2.4.Impact of ownership on the effect of the banking reform:Hypothesis 2

Before the reform,state-owned enterprises did not have to pay rent because they were supported by soft budget constraints.Further,the controlling shareholders of state-owned enterprises and non-state-owned enterprises had different residual claims on the firm and thus shareholders had no motive to pay rent.Managers of state-owned enterprises were essentially asset exploiters and had no efficient resources to pay rent.In this case,due to the impulse of investment and credit rationing restrictions,non-state-owned enterprises become the main entities paying rent to the commercial banks.All other things being equal,non-state-owned enterprises that were willing to pay the rent had easier access to credit.

According to this analysis,China’s financial market has two significant characteristics:soft budget constraints and rent-seeking.Thus,if state-owned enterprises with lower earnings quality obtain more loans after the reform,this means that government aid mechanisms have had an effect,whereas if non-state-owned enterprises with lower earnings quality obtain more loans then they must be paying rent.According to Xue and Zhu(2010),the reform has not really changed the nature of ownership and state-owned enterprises and commercial banks have not changed their use of soft budget constraints.In the short run,there is still an institutional basis for rent-seeking by banks after the reform,as non-state-owned enterprises are still the main entities that pay rent.All other things being equal,commercial banks will loosen the restriction on the earnings quality of non-state-owned enterprises.This is summarized as hypothesis 2.

H2.After the reform,commercial banks require lower earnings quality from non-state-owned enterprises than state-owned enterprises.

3.Sample,variables and descriptive analysis

3.1.Sample

Our data covers all A-share listed companies with financial data for the period 1998-2010.4We calculate earnings quality using the direct cash flow statements method.Accurate accruals data in the statement of cash flows is only available from 1998,so the initial year of our study is 1998.Financial data and other annual data were obtained from the CSMAR and WIND databases.Data on non-state-ownedenterprises was sourced from the CCER database.We exclude all utilities and financial institutions and winsorize the major variables at the 1%and 99%levels.

We investigate the impact of the financial reform on loan allocation to study whether the effect of ownership on loan allocation changes with an institutional change.Restricted by the measurement of earnings quality,we choose listed companies in the period 2001-2003 before the reform,and divide the period of our study of 2001-2009 at 2004 to obtain two stages,the pre-reform period from 2001 to 2003 and the post-reform period from 2005 to 2009.

3.2.Variables

(1)Bank loans

We use new short-term loans(Dls),new long-term loans(Dll)and new total loans(Dlt)to measure loan allocations,where Dls equals the difference between firm i’s closing and initial short-term loan balances divided by total assets,Dll equals the difference between firm i’s closing and initial long-term loan balances added to longterm loans of a maturity of less than 1 year divided by total assets,and Dlt equals the sum of Dls and Dll.

(2)Earnings quality

We use the modified Dechow-Dichev(2002,hereafter DD)measure to capture the quality attribute of main operating profits.We calculate 2001-2009 accrual quality using the relevant accounting information for rolling 5-year windows during 1998-2010:

where TCAi,t:firm i’s total current accruals in year t=(MOPi,t-CFOBTi,t)5The foreign literature calculates CFO as earnings before extraordinary items less total accruals.However,data on earnings before extraordinary items is not available before 2003 in China,so we use operating profit as a substitute and adjust operating cash flow to pretax CFO to be consistent with earnings.;CFOBTi,t:cash flow from operations adjusted by tax in year t=(CFOi,t-IncomeTaxReturns+IncomeTaxExpense);AVASSETi,t:firm i’s average total assets in year t and t-1;ΔREVi,t:firm i’s change in revenue between year t and t-1;PPEi,t:firm i’sgrossvalueofproperty,plantandequipmentinyeart;EQ:thenegativestandarddeviationoffirmi’sestimated residuals from(I)and EQ=-σ(^εi,t)(large(small)values of EQ corresponding to good(poor)earnings quality). (3)External financing dependence

According to Rajan and Zingales(1998)and Xue and Zhu(2010),we modify external financing dependence to measure a firm’s external financing requirements:

whereCAPXit:firmi’scapitalexpenditureinyeart,whichisequaltothesumofnewlong-terminvestment,fixed assets,intangible assets and other long-term assets;and CFOit-1:firm i’s lagged operating cash flow in year t.

(4)Ownership

According to previous research,companies with different ownership types have a different loan structure. We thus code state-owned enterprises as 0 and non-state-owned enterprises as 1.

(5)Control variables

Lagsize is the natural log of firm i’s lagged total assets.Gruber and Warner(1977)and Ang et al.(1982)find that bankruptcy costs as a percentage of a firm’s value reduce with increasing firm size,because large firms are more inclined to diversify,which leads to a lower risk of bankruptcy.Empirical studies also find that leverage is greater in large firms(Rajan and Zingales,1995).Other studies suggest that small firms have higher agency costs,a higher adverse selection cost of public financing(Smith,1977)and prefer short-term loans,which means that the size and leverage of small firms may be negatively related.

Lagroe is lagged return on equity.Financing order theory(Myers,1984;Myers and Majluf,1984)suggests that due to asymmetric information and transaction costs,firms prefer retained earnings when sourcing capital.Thus,a firm’s current profitability is important in measuring capital structure and a firm with higher earnings quality has less loans.However,trade-of ftheory suggests that when the marginal cost(bankruptcy costs and agency costs between shareholders and creditors)is equal to the marginal revenue(tax shields to decrease the constraints of cash flow and the information cost relative to equity financing)of debt financing,the firm maximizes its value and a firm with a higher pro fitability has more loans.Gonzalez and Gonzalez(2008)state that in countries with weak property rights protection, firms face higher external financing costs and follow financing order theory,although trade-o fftheory is more suitable in countries with good property rights protection.

Laglev is the lagged ratio of debt to total assets.Morris(1992) finds that long-term loans help firms to postpone bankruptcy,thus overleveraged firms prefer long-term loans.Stohs and Mauer(1996)suggest that a high ratio of long-term loans helps to increase a firm’s value.Leland and Toft(1996)show that a firm’s leverage depends on its debt maturity,where firms with a lower asset-liability ratio access short-term loans more easily. Dennis et al.(2000)found that a firm’s leverage has a close relationship with debt maturity.Others studies find that firms with a lower asset-liability ratio have to pay more cash in the future and face higher liquidity risk.

Laggrow is the lagged sales growth rate.A firm with higher growth opportunities has more flexibility in its future investment,and managers may choose investment projects that benefit shareholders but harm creditors.Myers(1984)suggests that firms borrow short-term loans to reduce agency costs,thus short-term loans will be positively related to growth and long-term loans will be negatively related to investment.However,Titman and Wessels(1988)consider that growth is the added value of firm’s assets and cannot be collateral or create tax revenue.

Table 1Variable definitions.

Lagfix is the lagged ratio of fixed assets to total assets.Scott(1972)and Myers and Majluf(1984)suggest that managers may benefit from selling collateral and the more managers can use collateral assets,the more opportunistic their behavior.Jensen and Meckling(1976)and Myers(1977)suggest that in a firm with higher leverage,managers are more likely to invest in projects that may harm creditors.Collateral helps to restrict borrowers from investing in higher risk projects and manager’s non-pecuniary compensation demands may lead to a positive relationship between collateral and debt levels.

Table 2Descriptive statistics before and after financial reform.

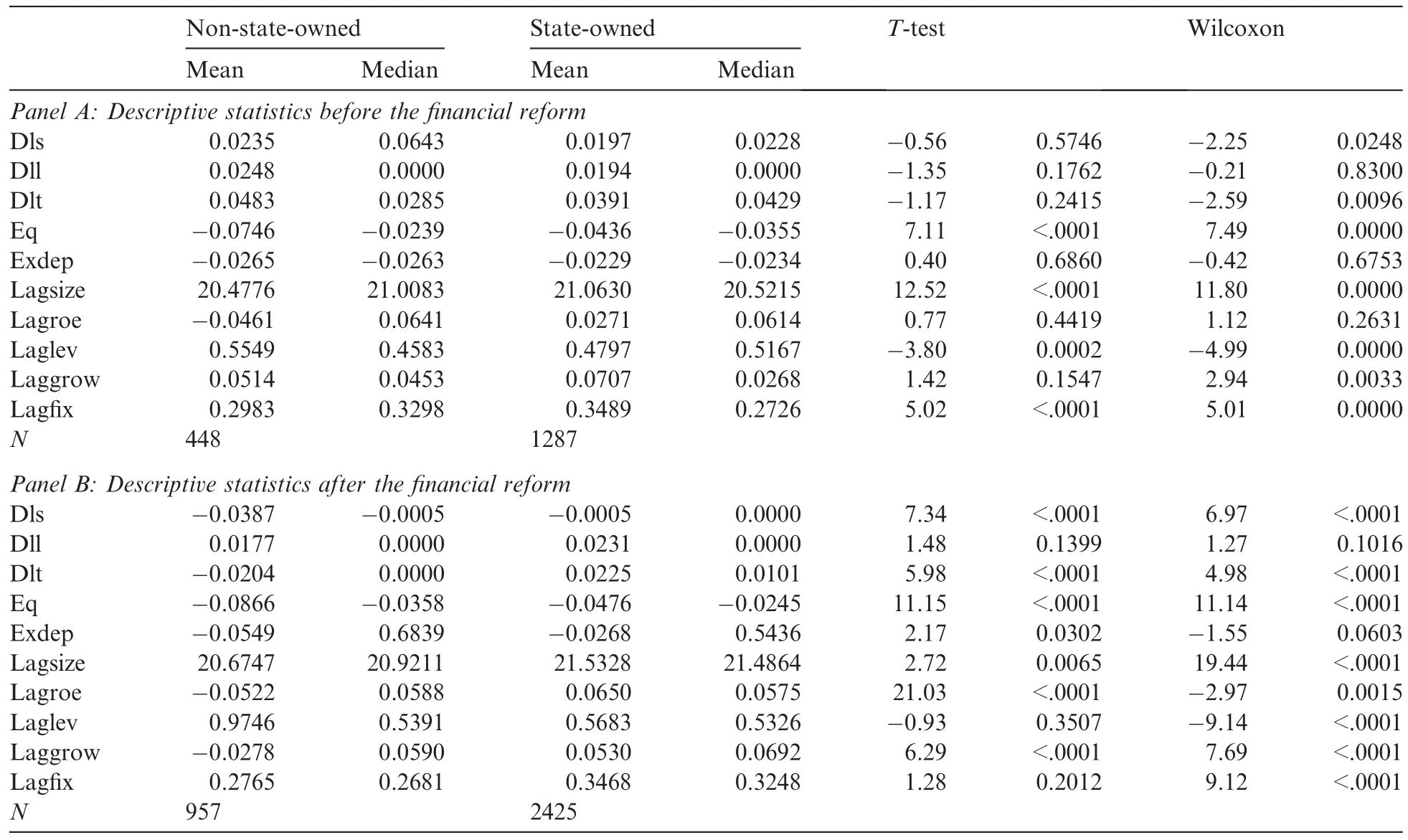

Table 3Descriptive statistics for state-owned and non-state-owned enterprises before and after the financial reform.

Table 4Impact of the banking system reform on loan allocation.

Following the literature,we also include year and industry dummies,and the district corruption index(Xie and Lu,2005)6The National Banking corruption index is 4.17.The index for northern China is 4.97,for western China is 4.71,for central China is 4.39,for southern China is 4.05,for northeastern China is 3.70 and for eastern China is 3.07(Xie and Lu,2005).as control variables.Table 1 presents the definitions of the variables.

3.3.Descriptive statistics

Table 2 reports descriptive statistics for the variables in the analysis before and after the financial reform. The mean and median values of new short-term loans(Dls)decrease significantly after the financial reform. The mean value of Dls decreases from 0.0199 to-0.0121,and the median value decreases from 0.0145 to 0.The mean and median values of new long-term loans(Dll)also decrease after the financial reform,with the median value decreasing significantly.Influenced by new short-term loans and new long-term loans,the mean and median values of new total loans also decrease significantly after the financial reform.

After the reform,the mean and median values of earnings quality(Eq)decrease significantly from-0.0518 and-0.0262 to-0.0592 and-0.0298,respectively.The mean and median values of external financial dependence(Exdep)decrease significantly from-0.0249 and-0.0258 to-0.0363 and-0.0413,respectively.After the reform,size and leverage are significantly higher and growth and fixed assets are significantly lower.These statistical results indicate that after the reform,the external financing of firms was significantly lower,with fewer loans,especially short-term loans.This indicates that short-term loans are more vulnerable to the impact of external environmental fluctuations.

Table 3 reports the descriptive statistics for the variables for state-owned and non-state-owned enterprises before and after the financial reform.Panel A reports the descriptive statistics before the reform and Panel Breports the descriptive statistics after the reform.Before the reform,the mean and median values of new shortterm loans(Dls)for state-owned enterprises are significantly lower than for non-state-owned enterprises.The values of new long-term loans and new total loans for state-owned enterprises are also lower than that for non-state-owned enterprises.This statistical result indicates that before the reform,short-term loans and long-term loans were complementary.The mean and median values of earnings quality(Eq)of state-owned enterprises are significantly higher than those of non-state-owned enterprises.There is an insignificant difference in the external financial dependence(Exdep)of state-owned and non-state-owned enterprises.

Post-reform,the values of new short-term loans and new total loans of state-owned enterprises is signif icantly higher than that of non-state-owned enterprises.There is an insignificant difference in long-term loans between state-owned and non-state-owned enterprises,which means that soft budget constraints are still in force after the reform.The mean and median values of earnings quality(Eq)of state-owned enterprises are still significantly higher than those of non-state-owned enterprises.There is still an insignificant difference in the external financial dependence(Exdep)of state-owned and non-state-owned enterprises.This result indicates that the earnings quality of state-owned enterprises is significantly higher during 2001-2009 than that of non-state-owned enterprises,and thus the reform has significantly improved the short-term credit market.

4.Results

4.1.Impact of the banking system reform on loan allocation

We use model(1)to analyze the variance in the impact of earnings quality on loan allocation between stateowned enterprises and non-state-owned enterprises:

Table 5Impact of the banking system reform on loan allocation to state-owned enterprises.

DlsDllDlt

Table 6Impact of the banking system reform on loan allocation to non-state-owned enterprises.

Table 4 reports the results of model(1)testing the variance in the impact of earnings quality on loan allocation before and after the reform.We find that before the reform earnings quality has a significant positive influence on new short-term loans and a significant negative influence on new long-term loans,which due to the substitutability of soft budget constraints means that earnings quality has no significant influence on new total loans.After the reform,the strength of the positive relationship between earnings quality and loans increases.The results in Table 4 indicate that the banking system reform has improved the efficiency of financial resource allocation and that earnings quality has had an incremental influence on credit loans.

Table 5 reports the results of model(1)testing the impact of state-owned enterprises’earnings quality on loan allocation before and after the reform.After the reform,the positive relationship between the earnings quality of state-owned enterprises and new short-term loans,new long-term loans and new total loans is enhanced.The results in Table 5 indicate that the banking system reform has improved credit allocation and tightened budget constraints.

Table 6 reports the results of model(1)testing the impact of the earnings quality of non-state-owned enterprises on loan allocation before and after the reform.After the reform,the relationship between the earnings quality of non-state-owned enterprise and new short-term loans,new long-term loans and new total loans does not change significantly.Combined with the results in Table 5,the reform appears to have had a greater impact on state-owned enterprises than non-state-owned enterprises,which provides preliminary evidence to verify Hypothesis 2.

4.2.Impact of ownership on the effect of the banking system reform

To further analyze the impact of the banking system reform on financial resource allocation,we include the Soe ownership variable(equal to 1 for non-state-owned enterprises)in our model:

Table 7 reports the impact of ownership on the effect of the banking system reform.When the ownership variable is included,the impact of the reform on credit resources becomes significantly negative and the postreform impact of the interaction between earnings quality and ownership on short-term loans,long-term loans and total loans is-0.2,-0.0232,and-0.2233.This means that the effect of the banking system reform on earnings quality has been lower in non-state-owned enterprises than in state-owned enterprises.These results show that commercial banks and non-state-owned enterprises have not reduced their rent-seeking since the reform.

The foregoing results are reported with White-adjusted standard errors.We also conducted several additional tests.We repeated the tests using the Jones model(Jones,1991),substituting earnings predictability(Lev,1983;Ali and Zarowin,1992;Francis et al.,2002)for earnings quality,using cash from borrowing from the cash-flow statement as total loans and using the sample year 2001 only.In addition,we repeated the tests using Tobin’s Q to measure a firm’s growth opportunities,ROA to measure a firm’s profitability and the natural logarithm of total sales to measure size.The results do not change in any of these additional tests and we do not report them due to space limitations.

Table 7Impact of ownership on the effect of the banking system reform.

5.Conclusion

This paper investigates credit allocation before and after the 2003 banking system reform to analyze the interactive influence of government,commercial banks,state-owned enterprises and non-state-owned enterprises on credit allocation.We find that the banking system reform has enhanced the role of earnings quality in the credit markets and eased the budget constraints of state-owned enterprises.Further analysis implies that,due to the influence of rent-seeking,banks have relaxed the earnings requirements of non-state-owned listed companies.

The practical implication of these findings is that improving credit allocation efficiency is not a matter of a simple policy choice,but is the result of institutional design.In the long run,further research is needed on the game theory of government,commercial banks,state-owned enterprises and non-state-owned enterprises in light of the stock-liquidity reform and the deeper financial system reform,with a focus on the influence of government governance on credit allocation.

Acknowledgements

This paper has benefited greatly from the comments and suggestions of the Executive Editor and two anonymous referees.We are thankful to Professor Qiang Xinrong from Xiamen University for her comments and suggestions at the 5th Symposium of China Journal of Accounting Research 2011.All remaining errors are our own.This paper was supported by the Jiangsu Province University Philosophy Social Science Fund Project entitled“Local Government Governance-Earnings Quality and Credit Allocation”(Grant No.: 2011SJD630055).

Akerlof,George A.,Romer,1993.Looting:the economic underworld of bankruptcy for profit.Brookings Papers on Economic Activity 98/2,1-60.

Ali,A.,Zarowin,P.,1992.The role of earnings levels in annual earnings-returns studies.Journal of Accounting Research 30,286-296.

Ang,J.,Chua,J.,McConnell,J.,1982.The administrative costs of corporate bankruptcy:a note.Journal of Finance 37(March),219-226.

Aoki,Okuno,2005.Comparative Institutional Analysis of the Economic System.Chinese Development Publisher(in Chinese).

Berglof,Erik,Roland,Gerard,1995.Soft budget constraints and credit crunches in financial transition.Journal of Japanese and International Economies 9,354-375.

Brandt,L.,Li,H.,2003.Bank discrimination in transition economics:ideology,information,or incentives?Journal of Comparative Economics 31,387-413.

Chow,G.L.,2008.Earnings Quality and Cost of Capital.Ph.D.Thesis,Shanghai University of Finance(in Chinese).

Cull,R.,Xu,L.,2005.Institutions,ownership,and finance:the determinants of profit reinvestment among Chinese firms.Journal of Financial Economics 77,117-146.

Dechow,P.,Dichev,I.,2002.The quality of accruals and earnings:the role of accrual estimation errors.Accounting Review 77 (Supplement),35-59.

Dennis,S.,Nandy,D.,Sharpe,I.G.,2000.The determinants of contract terms in bank revolving credit agreements.Journal of Financial and Quantitative Analysis 35,87-110.

Fang,J.X.,2010.Non SOEs:really facing banking lending discrimination?Management World 11,123-131(in Chinese).

Francis,J.,LaFond,R.,Olsson,P.,Schipper,K.,2002.The Market Pricing of Earnings Quality.Working Paper,Duke University, University of Wisconsin and the FASB.

Francis,J.,LaFond,R.,Olsson,P.,Schipper,K.,2003.Earnings Quality and the Pricing Effects of Earnings Patterns.Working Paper, Duke University,University of Wisconsin and the FASB.

Francis,J.,Khurana,K.,Pereira,R.,2005.Disclosure incentives and effects on cost of capital around the world.Accounting Review 80, 1125-1162.

Gao,S.,Schaffer,M.E.,1998.Financial Discipline in the Enterprise Sector in Transition Countries:How Does China Compare?Center for Economic Reform and Transition Discussion Paper:98/1,Heriott-Watt University,Edinburgh.

Gonzalez,Victor M.,Gonzalez,Francisco,2008.Influence of bank concentration and institutions on capital structure:new international evidence.Journal of Corporate Finance 4(14),363-375.

Gruber,M.,Warner,J.,1977.Bankruptcy costs:some evidence.Journal of Finance 32,337-347.

Jaffee,Dwight M.,Russell,Thomas,1976.The imperfect information,uncertainty,and credit rationing.The Quarterly Journal of Economics 90(4),651-666.

Jensen,M.C.,Meckling,W.,1976.Theory of the firm:managerial behavior,agency costs and capital structure.Journal of Financial Economics 3,305-360.

Jiang,W.,Li,B.,2006.Institutional environment,state ownership and lending discrimination.China Financial Research 11,116-126(in Chinese).

Jones,J.,1991.Earnings management during import relief investigations.Journal of Accounting Research 29,193-228.

Kornai,J.,1980.Economics of Shortage.Amsterdam,North Holland.

Kornai,Ja´nos,Maskin,Eric,Roland,Ge´rard,2003.Understanding the soft budget constraints.Journal of Economic Literature XLI, 1095-1136.

Leland,H.E.,Toft,K.B.,1996.Optimal capital structure,endogenous bankruptcy,and the term structure of credit spreads.Journal of Finance 51,987-1019.

Lev,B.,1983.Some economic determinants of the time-series properties of earnings.Journal of Accounting and Economics,31-38.

Lin,Y.F.,Cai,F.,Li,Z.,1997.Full information and Reform of SOEs.Shanghai People’s Publisher.

Lin,Y.F.,Cai,Li,Z.,1994/1999.Chinese Miracle:Development strategy and economic reform.Shanghai People’s Publisher(1999 Revised Edition).

Lin,Y.F.,Liu,M.X.,Zhang,Q.,2004.Policy burden and enterprises’soft budgetary binding:a case study from China.Management World 8,34-45(in Chinese).

Morris,J.R.,1992.Factors Affecting the Maturity Structure of Corporate Debt.Working Paper,University of Colorado at Denver.

Myers,S.,1977.Determinants of corporate borrowing.Journal of Financial Economics 9,147-176.

Myers,S.,1984.The capital structure puzzle.Journal of Finance 39,575-592.

Myers,S.,Majluf,N.,1984.Corporate financing and investment decisions when firms have information investors do not have.Journal of Financial Economics 13,187-221.

Rajan,R.G.,Zingales,L.,1995.What do we know about capital structure?Some evidence from international data.Journal of Finance 50 (5),1421-1460.

Rajan,R.,Zingales,L.,1998.Financial dependence and growth.American Economic Review 88,559-586.

Scott,D.,1972.Evidence on the importance of financial structure.Financial Management 1,45-50.

Smith,C.,1977.Alternative methods for raising capital:rights versus underwritten offerings.Journal of Financial Economics 5,273-307.

Stohs,M.H.,Mauer,D.C.,1996.The determinants of corporate debt maturity structure.Journal of Business 69,279-312.

Sun,Z.,Liu,F.W.,Li,Z.Q.,2005.Market development,government influence and corporate debt maturity structure.Economic Research Journal 5,52-63(in Chinese).

Titman,S.,Wessels,R.,1988.The determinants of capital structure choice.Journal of Finance 43,1-19.

Williamson,Stephen D.,1986.Costly monitoring,financial intermediation,and equilibrium credit rationing.Journal of Monetary Economics 18,159-179.

Wu,J.,Bai,Y.,2009.The impact of China’s banking reform on the soft budget constraint of SOEs.China Financial Research 10,180-192.

Xie,P.,Lu,L.,2005.The Economic Analysis of Chinese Financial Corruption.Zhongxing Publisher.

Xue,Y.K.,Zhu,X.L.,2010.Institutional changes,earnings quality and debt contract empirical evidence from the Chinese banking system reform.China Accounting and Finance Review 3,57-106(in Chinese).

Zhang,M.,Zhang,S.,Sheng,H.,Wang,C.,2010.Political connections and credit resource allocation efficiency.Management World 11, 143-153(in Chinese).

4 January 2012

*Corresponding author at:Nanjing University of Finance and Economics,Wenyuan Road 3,Xianlin,Xixia District,Nanjing,China.

E-mail address:xiulizhuzhu@126.com(Z.Xiuli).

杂志排行

China Journal of Accounting Research的其它文章

- The role of cross-listing,foreign ownership and state ownership in dividend policy in an emerging market

- Internal corporate governance and the use of IPO over-financing:Evidence from China

- An empirical study of the effect of venture capital participation on the accounting information quality of IPO firms