Nod of Approval For Black Lending

2011-10-14LIUYUNYUN

Nod of Approval For Black Lending

Private lending, once obscure and operated underground, gets an unofficial go-ahead from the Central Government

When it comes to underground or black market lending, a major source of fnancing for small and medium-sized business owners, the Chinese Government had taken much the same approach as a legendary hero combating a mythological hydra: decapitating the many heads in an effort to slay the beast. Even now, as the government steps up efforts to tighten credit, the heads of the underground lending realm are sprouting up as fast as they are being cut off, causing China’s leaders to rethink their strategy.

Remarks recently made by a central bank offcial have been regarded as the government’s official recognition of unofficial private lending, according to Xinhua News Agency.

“Private lending is a beneficial and necessary complement to formal financing channels,” the offcial said.

These alternative, and illegal, channels meet certain fnancial needs of various social institutions, especially small and mediumsized enterprises (SMEs) and agriculturerelated sectors, said the central bank offcial. Private lending is also conducive to forming a multi-tiered credit market.

With the rapid development of small-loan companies, the government should regard them as professional lenders, and they should be covered under the government’s monitoring system. In the meantime, the offcial urged a crackdown on crimes like illegal fund raising, loan shark practices and money laundering.

The interest rate of any private loans should not exceed four times that of bank loans, said the offcial, citing an existing rule set by the Supreme People’s Court. He said any rate exceeding this amount is exorbitant and is not protected by law. The disputes stemming from the interest rate should be brought to the court which will determine the effectiveness of the loan contract between the two parties involved.

“Relative departments are studying, trying out and improving a tracking and monitoring system on private lending to provide more comprehensive information for economic decision making and macro-economic control,” said the offcial.

The remarks came amid a credit crunch in the eastern city of Wenzhou, an economic hub for Chinese SMEs, which has caused a number of industrial bosses and business owners to leave the city and even the country in some extreme cases.

The central bank has raised benchmark interest rates three times this year and hiked the reserve requirement ratio for lenders six times, making it diffcult for small businesses to borrow from banks.

Many small businesses in Wenzhou turned to high-interest black lending market since they couldn’t get bank loans after the government tightened lending to clamp down on inflation. However, due to the bleak international and domestic market conditions, entrepreneurs later found they could not repay the loans. According to a21st Century Business Heraldreport, by the end of October this year, a total of 228 entrepreneurs had run away and nine committed suicide. The number is on the rise.

Analysts believed the central bank offcial’s remarks are meant to track those loans and standardize them so the interests of both sides can be properly protected.

Policy background

China International Capital Corp. Ltd. issued a research report on China’s private lending in October, noting that private lending is expected to reach 3.8 trillion yuan ($584.61 billion) in 2011, rising 38 percent year on year. This is equivalent to 7 percent of all bank loans.

The private lending business has attracted a diverse cohort of participants: guarantee companies, pawn shops, small loan businesses, investment and leasing companies, private enterprises and individuals with deep pockets.

The loans in the underground system often come with exorbitant interest rates of up to 70 percent. Private lending crises, with capital fund breakdowns of so-called guarantee companies, are increasing in frequency. A growing number of owners of SMEs have begun to abandon their operations and hometowns, taking to the road to avoid loan sharks.

Zhou Dewen, President of the Wenzhou Small and Medium-Sized Enterprise Business Development and Promotion Association, said the interests of lenders and borrowers could only be protected and come under government monitoring if their conduct is legalized.

Strapped for cash and shunned by big banks, SMEs are often forced into the arms of private lenders who provide necessary funding at a hefty interest rate.

“I borrowed 700,000 yuan ($107,692) from other businessmen, and the monthly interest rate is 5.8 percent. The sum was just to get the production line started,” said Liu Hao, a small furniture company owner in Guangzhou, south China’s Guangdong Province.

Liu said it has been hard to get loans from banks this year, and he got the money from his peers at a yearly interest rate as high as 60 percent. A bank loan would have come with an interest rate of 6.65 percent.

Yang Xiaoqiang, professor at the School of Law of Zhongshan University, said when companies need financing, they would first turn to legal financial institutions. China’s stringent money supply guidelines, however, make it diffcult to get that fnancing, especially with commercial banks favoring powerful state-owned enterprises over smaller, less predictable businesses. The big companies may be unable to pay back the loans, but they still have the government for support.

Many of China’s banks are steadfast in their approach to SMEs. Guaranteeing the bottom line is a priority, but saving small businesses from bankruptcy is not.

“We only support the companies we know well,” said Lu Xianzhi, a director of the loan department of a branch of Agricultural Development Bank of China in Jiangsu Province. “We take money from our depositors, and we must be responsible for them. We have rules when giving loans.”

Necessary lending

Knowing full well the favored treatment big businesses receive, small businesses know private lending is one, if not the only one, of their options to start up or stay afoat.

There are three ways to get private loans. The first is small credit companies. In the Pearl River Delta region the monthly interest rate is 2.5-3 percent with mortgage and 6.8-10 percent without mortgage. Lending from peers and business partners is another way. Borrowers could usually get loans at a 6-12 percent monthly interest rate. The third channel is underground banks whose source of capital is shrouded in mystery and deceit with risks of illegal money raising and money laundering.

Since it is hard to get loans from banks, many turn to underground banks or small loan companies for quick cash.

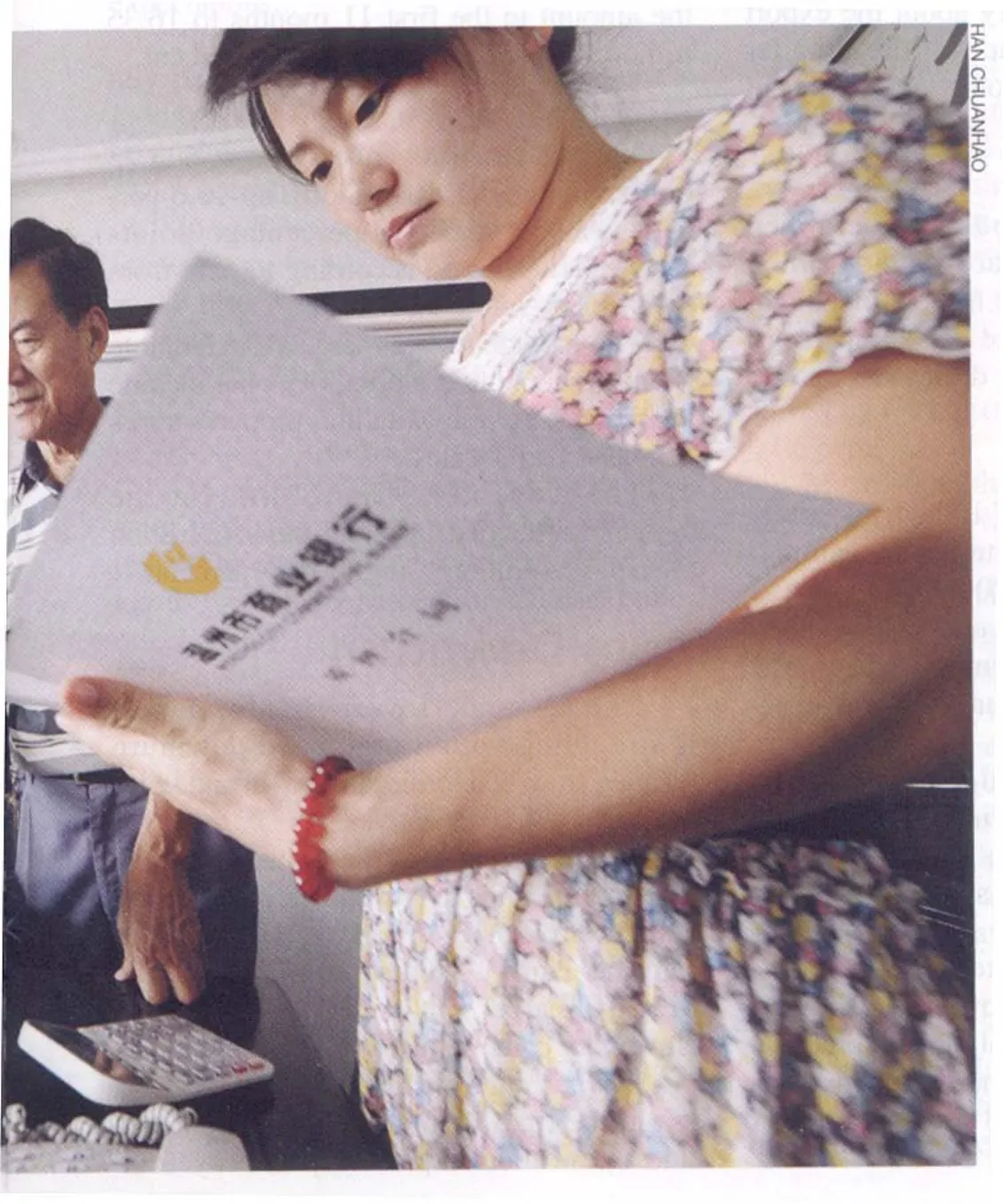

Niu Wei, marketing director for a start-up company, used a private lending frm to pay the down payment for her third apartment in Beijing. She had to make a down payment of 400,000 yuan ($61,538) in 30 days but only had 300,000 yuan ($46,153) on hand, including the money borrowed.

“I had already asked all my friends and family members, but still lacked 100,000 yuan ($15,380). Then a friend of mine recommended Creditease,” Niu said. Niu provided her personal ID, monthly salary certificate and the property ownership certificates. Within a week, she got what she wanted at an interest rate of 1.42 percent per month, 18 percent a year.

Big banks certainly have lower rates, but they have too many requirements, Niu said.“Most importantly, the private lender did not need a mortgage.”

Possible obstacles

In spite of the central bank’s good intention of taking pressure off small businesses, experts have their doubts about the effectiveness and feasibility of the new rule.

HAN CHUANHAO

“I cannot think of any economic equilibrium that justifes the four-times rate set by the central bank,” said Mao Yushi, a wellknown independent economist. Mao said the central bank should have made more research before it jumped to a conclusion.

The one-year loan interest rate of commercial banks is set at 6.56 percent, while the rate of private lending ranges from 18 to 70 percent. Many private lenders borrow money from the banks and lend them to small business owners to take advantage of the rate difference. The central bank offcial stated that anyone who borrows money from banks and lends them at a higher rate would be convicted as a loan shark and punished. But Guo Tianyong, professor and director of the Research Center of the Chinese Banking Industry of the Central University of Finance and Economics, said the issue needs to be discussed thoroughly before further action is taken. He said it is natural for people to chase profts whether it is through selling products or loaning money. Now that there are people who would like to borrow money from private lenders, it proves that private lending has its market.

Therefore, as Guo contended, it is unfair for the government to punish those engaged in arbitrage.

It’s not just individuals and SMEs that need private lending to get loans. Many holding debts are successful entrepreneurs themselves, and some wealthy people put their life savings into private fnancing institutions to lend it at higher rates to businesses to get a windfall.

With many in-debt SME bosses feeing their financial and commercial obligations, the depositors are fretful—the money that they have toiled for years or generations to earn has now vanished. Some individuals mortgaged their houses to banks and used the money from banks to join the private lending business. Some put their pensions in the hands of private lenders. The government has so far had no specifc rules and regulations on protecting their legitimate rights.

The extraordinarily high rate makes interest a huge cost for SMEs. Even if the interest rate for private lending is 24-28 percent, as the central bank offcial described as legal, SMEs may still lose money, as a majority of their turnover goes to the pocket of private lenders.

Legalization comes with a cost, as lenders will be subject to a series of supervision conditions. For instance, they might have to pay taxes for the interest they earn. If the private lenders have no intention of receiving government supervision, they might swiftly turn underground again, which might bring negative infuences on the government’s decision making.